{kind=link}

Last Updated on October 17, 2021 by Constitutional Militia

The author wishes to thank the National Alliance for Constitutional Money for its support and Dr. Lawrence M. Parks, Executive Director of the Foundation for the Advancement of Monetary Education, for his encouragement in the preparation of this article.

I. INTRODUCTION

Over the past several decades, many Americans have considered inflation to be one of this country’s most intractable economic, social, and political problems—and rightly so. But few people have actually studied works that describe the history of inflation in this and other societies,[1] that explain its causes and effects,[2] or that propose effective policies to eradicate it.[3] Instead, the vast majority obtains information on this subject from the government and the media—the performance of which in explaining inflation draws into serious question the competence, if not the motives, of leading political figures and commentators.[4] Therefore, not surprisingly, few Americans know even how to define inflation correctly. To most, “inflation” simply imports general increases in the prices of goods and services, without specifying the reason for those increases.

Even a source no more technical than a layman’s dictionary better separates cause and effect in its treatment of “inflation,” defining it as “an increase in the volume of money and credit relative to available goods resulting in a substantial and continuing rise in the general price level.”[5] More precisely still, Ludwig von Mises defined inflation as any increase in the quantity of money “not offset by a corresponding increase in the need for money . . . , so that a fall in the objective exchange-value of money must occur.”[6] Murray Rothbard further refined the definition of inflation as “the process of issuing money beyond any increase in the stock of specie [i.e., silver and gold],” explaining that, although increases in the stock of specie can raise the prices of goods, they “do not constitute an intervention in the free market, penalizing one group and subsidizing another” or “lead to the processes of the business cycle.”[7]

Once issuing money beyond any increase in the stock of specie is understood to be the key operational element in inflation, anyone can see that the chief source of inflation in the contemporary United States is the ability of the Federal Reserve System to generate an endless stream of paper currency Federal Reserve Notes. These Notes are purportedly a legal tender for all debts, public and private,[8] supposedly an “obligation of the United States,”[9] and not redeemable in silver or gold coin or bullion by anyone other than the twelve Federal Reserve regional banks.[10] Surprisingly, though, next to no one asks whether this ability is constitutional. People seem naturally to assume that inflation—and, perhaps one of these days,—deflation is merely the result of some unfortunate, but innocent and correctable mistakes that have cropped up in administering the Federal Reserve System; that reform is simply a matter of revising the structure and regulation of the system, and hiring managers more competent than those who have served in the past. Next to no one asks whether inflation is a more deep-seated problem that can be addressed and resolved only by returning to first principles both of monetary and banking economics and of constitutional law. Why is the Constitution, which in other contexts is easily—indeed, flippantly—invoked to advance “rights” unheard of the day before their assertion, not applied rigorously to an institution the actions of which are pregnant with such serious consequences for the economy of the United States? Is the Constitution simply irrelevant to contemporary issues of money and banking? Or have all these issues been settled in favor of the legality of the Federal Reserve System and its irredeemable paper currency? Surely there is a pressing need to answer these questions.

II. THE ILL DEFINED DOLLAR

Nobel Laureate economist James Buchanan has condemned America’s present monetary and banking systems as intellectually indefensible.[11] And in the monetary statutes of the United States alone, the incomprehensibility, if not irrationality, of the system stands out starkly, even at the most basic level: the definition of the “money of account.” Under present law “United States money is expressed in dollars.”[12] Moreover, all “United States coins and currency (including Federal reserve notes . . .) are legal tender for all debts, public charges, taxes and dues.”[13] Thus, all coins and currency, including Federal Reserve Notes, that are expressed in dollars are both money and legal tender. For this reason, accurately defining the noun “dollar” is mandatory in order to know what is “United States money” and what constitutes “legal tender for all debts, public charges, taxes and dues.” Unfortunately, the monetary statutes do not define the term dollar in an intelligible fashion.

A. Paper Currency

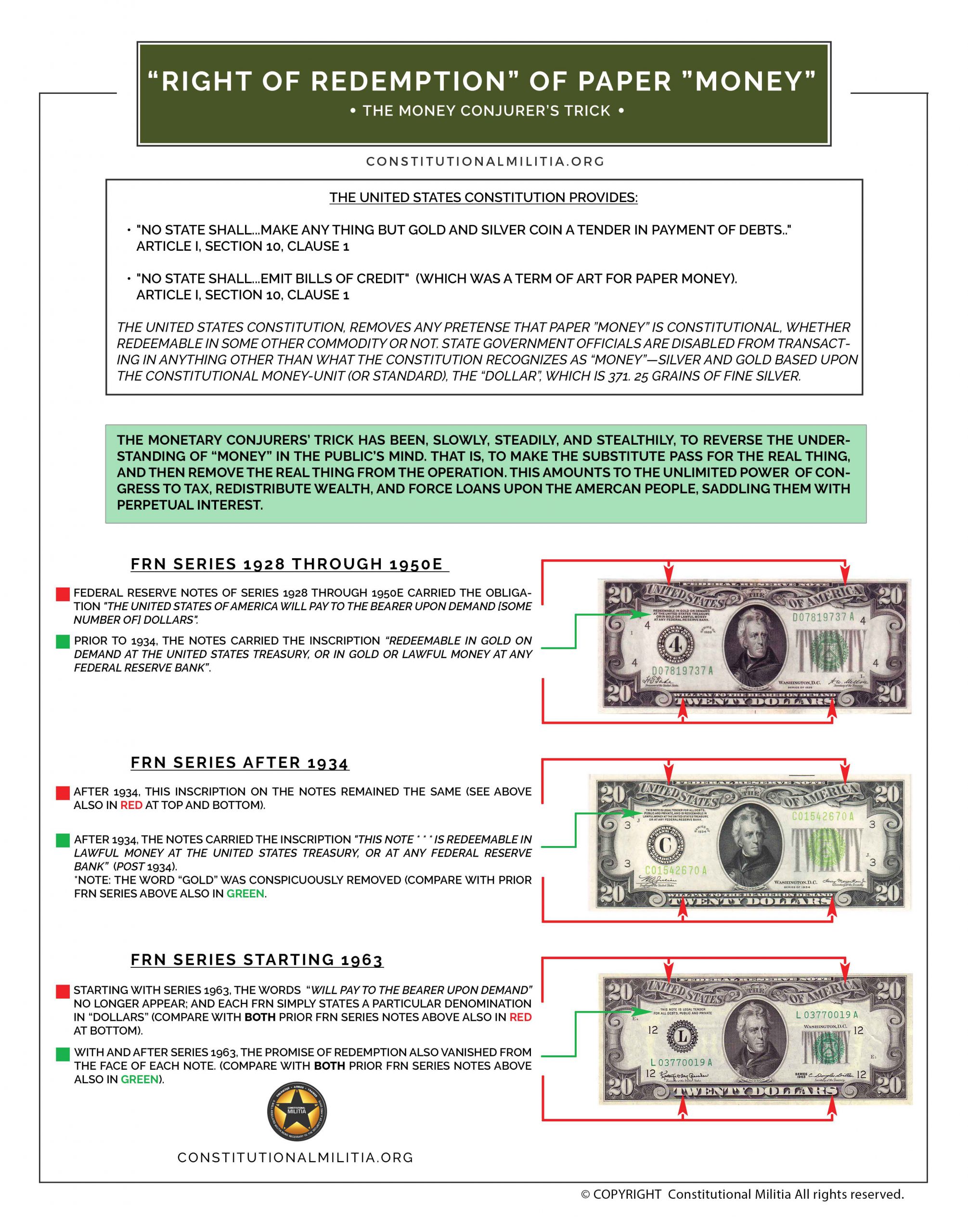

It is a mistake to associate the noun “dollar” with the Federal Reserve Note (“FRN”) dollar bill, engraved with the portrait of President George Washington. No statute defines or has ever defined the one-dollar FRN as the dollar or even as a species of dollar. Moreover, the United States Code provides that FRNs “shall be redeemed in lawful money on demand at the Treasury Department of the United States . . . or at any Federal Reserve bank.”[14] Thus, FRNs are not themselves even “lawful money”; otherwise, they would not be “redeem[able] in lawful money.” Moreover, FRNs are not lawful money imply perforce of their being “legal tender.” Originally, Section 16 of the Federal Reserve Act provided that FRNs “shall be redeemed in gold on demand at the Treasury Department of the United States . . . , or in gold or lawful money at any Federal reserve bank.”[15] In 1933, Congress provided that “all . . . coins and currencies heretofore or hereafter coined or issued by or under the authority of the United States shall be legal tender for all debts public and private.”[16] Apparently, however, Congress itself questioned whether this applied to FRNs because it later explicitly declared “Federal Reserve notes [to be] legal tender for all debts, public and private, public charges, taxes, duties, and dues.”[17] This, however, did not stop Congress from then continuing the requirement that FRNs “shall be redeemable in lawful money on demand at the Treasury Department . . . or at any Federal Reserve bank.”[18] And if FRNs are not even lawful money, it is inconceivable that they are somehow dollars, the very units in which all “United States money is expressed.”[19]

People are confused on this point because of the insidious manner in which FRNs evolved—actually, degenerated is a more appropriate verb—from the late 1920s until today. FRNs of Series 1928 through Series 1950E carried the obligation “THE UNITED STATES OF AMERICA WILL PAY TO THE BEARER ON DEMAND [some number of] DOLLARS,” and the inscriptions “REDEEMABLE IN GOLD ON DEMAND AT THE UNITED STATES TREASURY, OR IN GOLD OR LAWFUL MONEY AT ANY FEDERAL RESERVE BANK” (pre-1934); or “THIS NOTE . . . IS REDEEMABLE IN LAWFUL MONEY AT THE UNITED STATES TREASURY, OR AT ANY FEDERAL RESERVE BANK” (post-1934). Starting with Series 1963, the words “WILL PAY TO THE BEARER ON DEMAND” no longer appeared, and each FRN simply stated a particular denomination in dollars. With and after Series 1963, the promise of redemption also vanished from the face of each note.[20] Thus, on their faces FRNs became, in the apt description of banking expert John Exter, an “IOU nothing” paper currency in terms of silver or gold. Indeed, contemporary FRNs merely declare, “THIS NOTE IS LEGAL TENDER FOR ALL DEBTS, PUBLIC AND PRIVATE,” with no reference to redemption at all—perhaps justifying, surely necessitating, the inscription on the reverse side of the bill, “IN GOD WE TRUST.” FRNs do remain statutory redeemable in lawful money.[21] But because redemption in gold has been outlawed for anyone other than Federal Reserve banks,[22] a nonbank holder of FRNs can expect to receive no more than base-metallic clad coins—that is, slugs.[23]

The devolution of FRNs from a paper currency redeemable in gold to one redeemable only in slugs is explicable economically and politically: To introduce the FRN as a new paper currency in 1913, the government had to tie it by a right of redemption to the circulating money of that day, gold coin.[24] And then, to transmogrify the FRN into a currency fit for limitless inflation, the government had to cut that tie to gold. However, the change in the mere language printed on FRNs and in their redeemability in gold could not transform that currency’s ultimate legal character. If FRNs were not dollars when they explicitly promised to pay in gold, or later merely in lawful money, they did not magically become dollars when they stopped explicitly promising to pay in anything at all.[25]

B. Coins

The situation with coinage is more complex, and thus, equally, if not more, confusing. The United States Code provides for three types of coinage denominated in dollars: namely, base-metallic, gold, and silver coinage. The base-metallic coinage consists of “a dollar coin” weighing “8.1 grams”; “a half dollar coin” weighing “11.34 grams”; “a quarter coin” weighing “5.67 grams”; and “a dime coin” weighing “2.268 grams.”[26] All these coins are composed of copper and nickel.[27] The weights of the dime, the quarter, and the half dollar are in the correct arithmetical proportions to each other.[28] But the dollar is disproportionately light (or the other coins disproportionately heavy). This series of base-metallic coins, then, naturally raises the questions: Is the dollar a cupro-nickel coin weighing 8.1 grams? Or is it two cupro-nickel coins (or four or ten coins) collectively weighing 22.68 grams? Or is it both? Or is it neither, but something else altogether, to which the compositions and weights of these coins are irrelevant?

Similarly, the gold coinage consists of a “fifty dollar gold coin” that “weighs 33.931 grams, and contains one troy ounce of fine gold”; a “twenty-five dollar gold coin” that “contains one-half ounce of fine gold”; a “ten dollar gold coin” that “contains one fourth ounce of fine gold”; and a “five dollar gold coin” that “contains one-tenth ounce of fine gold.”[29] The fifty-dollar, twenty-five-dollar, and five-dollar coins are in the correct arithmetical proportions to each other. But the ten-dollar coin is not.[30] Therefore, is a dollar one-fiftieth or one-fortieth of an ounce of gold? Or both? Or neither? And what is the logical, economic, or other rational relationship between a dollar containing 8.1 grams of copper and nickel, and a dollar consisting of 0.679 grams of gold alloy?[31]

Finally, the silver coinage consists of a coin that is inscribed “One Dollar,” weighs “31.103 grams,” and contains one ounce of “.999 fine silver.”[32] What are the rational relationships (if any) among this dollar of 31.103 grams of .999 fine silver, a dollar containing 0.679 grams of gold alloy, and a dollar containing 8.1 grams of base metals? Obviously, these are not the amounts of the various metals that exchange against each other in the free market—that is, the different weights of different metals do not reflect equivalent purchasing powers. So, on what theory are each of these disparate weights of different metals with disparate purchasing powers equally dollars?

C. The Role of the Secretary of the Treasury

The United States Code provides no answer to this perplexing question. Indeed, it mandates that the question should not even be capable of being asked. For the Code commands that “the Secretary [of the Treasury] shall redeem gold certificates owned by the Federal reserve banks at times and in amounts the Secretary decides are necessary to maintain the equal purchasing power of each kind of United States currency.”[33] One need be no expert in currency transactions to know that a fifty-dollar gold coin has significantly more purchasing power than a fifty-dollar FRN or than fifty cupro-nickel dollars, and that a one-dollar silver coin has significantly more purchasing power than a one-dollar FRN or one cupro-nickel dollar. Thus, one need be no expert in administrative law to realize that the Secretary of the Treasury has defaulted on his obligation to keep all forms of United States currency at parity with each other—that is, to maintain a dollar of constant purchasing power, whether it be composed of gold, silver, base metals, or paper.[34] In addition, the concept of equal purchasing powers of all forms of United States coinage has a long statutory history from 1792 through 1900 to 1933.[35]

However, the Secretary’s default cannot be traced to a lack of power to perform his duty. For example, under the provisions of the United States Code:

With the approval of the President, the Secretary of the Treasury may (A) buy and sell gold in the way, in amounts, at rates, and on conditions the Secretary considers most advantageous to the public interest; and (B) buy the gold with any direct obligations of the United States Government or United States coins and currency authorized by law . . . .[36]

The Secretary may buy silver mined from natural deposits in the United States . . . that is brought to a United States mint or assay office within one year after the month in which the ore from which it is derived was mined.[37]

The Secretary may sell or use Government silver to mint coins . . . . The Secretary shall sell silver under conditions the Secretary considers appropriate for at least $1.292929292 a fine troy ounce.[38]

Except to the extent authorized in regulations the Secretary of the Treasury prescribes with the approval of the President, the Secretary may not redeem United States currency . . . in gold . . . . When redemption in gold is authorized, the redemption may be made only in gold bullion bearing the stamp of a United States mint or assay office in an amount equal at the time of redemption to the currency presented for redemption.[39]

Thus, the United States Code simply presents another unanswered question: Why has the Secretary of the Treasury failed “to maintain the equal purchasing power of each kind of United States currency”?[40]

In sum, the present monetary statutes do not define the noun “dollar” in an unique way. Instead of monetary law—which would seem to require clearly defined terms and rational relationships among them—the country’s present monetary code smacks of political psychosis, in which completely different things have the same name, things unequal to each other are treated as equivalent, and things that should have the same characteristics (e.g., equal purchasing powers) are quite different.

III. MODERN MONETARY MISUNDERSTANDINGS

Leading intellectuals have no more coherent conception of the dollar than do the people or Congress. For a prime example, in his introduction to William Harvey’s Coin’s Financial School, the well-reputed historian Richard Hofstadter excoriates Harvey:

Harvey’s version of the history of American money could hardly have been more misleading. His elaborate attempt to establish that the original monetary unit was a silver dollar, and that gold was “also made money” but that “its value was counted from the silver dollar” is nonsensical, as well as gratuitous. The original monetary unit was simply the dollar, circulated in a variety of pieces of both gold and silver.[41]

Obviously, however, Hofstadter never read (or understood) Section 9 of the Coinage Act of 1792, which explicitly refers to “DOLLARS or UNITS each to be of the value of a Spanish milled dollar as the same is now current, and to contain three hundred and seventy one grains and four sixteenth parts of grain of pure . . . silver,” not gold.[42] The act mandated a set of gold coins denominated “EAGLES,” which were not themselves “dollars,” but were “to be of the value of” so many “DOLLARS,” according to their weights of gold at the statutory exchange ratio of fifteen-to-one between silver and gold.[43] So, what Hofstadter derides as Harvey’s supposedly “misleading,” “gratuitous,” and even “nonsensical” interpretation is exactly what the statute provides in so many words! Is it any wonder, then, that in an atmosphere of such intellectual confusion and hubris, today’s monetary and banking systems have reached an impasse in which “nothing works,” and where “today’s predicament is beyond the means of any economic theory”?[44]

Apparently, however, nothing can be done, because the forces of the status quo are solidly entrenched politically. For example, James Buchanan recounted how in 1980 Ronald Reagan’s staff solicited suggestions as to what the President-elect could do “to give an indication that [his] was going to be an administration with a policy thrust.”[45] Buchanan advised Reagan to “appoint a presidential commission that would look into . . . the Federal Reserve authority,” because “[w]hat we have now . . . never would have been constitutionally approved, on any kind of rational calculus, no matter what the political system.”[46] In response to inquiries from Reagan’s staff, Buchanan delivered a short position paper to Reagan. But, Buchanan lamented,

Absolutely nothing happened. I never heard . . . one word from them. I found out months later, that they did consider the idea, but Arthur Burns [then-Chairman of the Board of Governors of the Federal Reserve System] . . . rejected it, and would not have anything to do with any proposal that would change the authority of the central banking structure you don’t even . . . raise it as an issue to be discussed.[47]

From this experience, Buchanan characterized “the barrier of bureaucratic interest in maintaining” the present monetary and banking system as “extremely strong.”[48] Others might have concluded that something beyond a merely “bureaucratic interest” drove Burns’ refusal to allow the issue to be ventilated.[49]

This perverse interest in not having the Federal Reserve System even discussed is propped up by public ignorance about money and banking. The average man has no conception of the difference between an FRN dollar bill that is merely exchangeable with some merchant in the market-place for unpredictably varying amounts of goods and services (generally less and less, as time goes by) and a dollar bill that is redeemable by law by the issuer for a fixed amount of precious metal. He does not realize that other than base-metallic coinage, which itself is merely exchangeable but not redeemable by law, the only exchange for FRNs he can demand by legal right from the national government is to set off some tax or other liability he owes that government.[50] And this set-off is possible only because FRNs are statutory “obligations of the United States,”[51] a designation that may be repealed at any time.[52] That is, FRNs amount merely to circulating tax-anticipation coupons, nothing more. Neither does the average man suspect that what he imagines is his money in his “deposit account” in some member-bank of the Federal Reserve System (or any other bank, for that matter) is, in the eye of the law, really a loan he has made to the bank, and the bank’s money.[53] Nor does the average man fathom the operations and consequences, if he even realizes the existence, of the “fractional-reserve” system on the basis of which his mis-named “deposits” are manipulated. This, of course, is no peculiar failing of contemporary Americans. When President Franklin D. Roosevelt declared a national bank holiday in 1933, he felt it necessary to use his first radio Fireside Chat to explain to the American people why the banks could not pay out all their deposits.[54] Roosevelt had no illusions about the ignorance of the public on that score.

To be sure, with the proper guidance, these issues are easily understood.[55] Rather than educate himself on such matters, however, the average man today swallows the propaganda line of the Department of the Treasury and the Federal Reserve System that money and banking are “technical” areas “too complicated” for voters and politicians to understand, better left to “experts” for management in accordance with the arcane theories of contemporary mathematical economics, and certainly too important to become issues in the superficiality, buffoonery, and hurly-burly of electoral campaigns. This self-imposed ignorance of the great majority of Americans explains the country’s responses to the three major monetary and banking collapses that have followed the creation in 1913 of the Federal Reserve System: the seizure of the people’s gold coins and termination of redemption of FRNs in gold domestically, in 1933; the termination of redemption of United States paper currency in silver domestically and internationally, in 1968; and the termination of redemption of FRNs in gold internationally, in 1971. Notwithstanding how radically destructive of the monetary system each one of these events (and especially their cumulative effect) has been, not one nor all of them together triggered a constitutional, or even a political, crisis comparable to those that occurred, with massive participation by the general public in the late 1700s, over ratification of the Constitution and its “hard-money” provisions; in the 1830s, over the recharter of the Second Bank of the United States; in the 1870s, over resumption of specie payments for the Civil War “Greenbacks”; in the 1880s and 1890s, over the so-called gold standard and free silver; or in the early 1900s, over the creation of a central bank.

IV. THE CONSTITUTION IGNORED

So, perhaps not surprisingly, the contemporary consensus seems to be that the Constitution somehow affirmatively grants the government (and the private parties behind the Federal Reserve System) unlimited powers over money and banking, and that questioning such an assumption is an exercise in futility, if not a species of intellectual “extremism.” For example, Geoffrey Brennan and James Buchanan say that “no country allows a totally free market in money, and none limits the governmental role to the definition of value of a monetary unit in support of a pure commodity standard.”[56] Murray Rothbard writes that “each nation-state . . . has . . . the unlimited right and power to create paper currency that will be legal tender in its own geographic area.”[57] James Dorn contends that “[p]resent U.S. monetary law incorporates . . . no constitutional limit binding the central bank [i.e., the Federal Reserve System] to a noninflationary path of money growth[,] . . . specifies no single objective for monetary policy[,] and lacks an enforcement mechanism to achieve monetary stability.”[58] And Henry Holzer argues that, at a minimum, a constitutional amendment is necessary to end monetary and banking manipulations by the government and its political clients.[59] Indeed, these ideas are shocking. For, if correct, they collectively describe a monetary and banking monopoly operated by a legally uncontrollable corporative-state banking cartel.

Notwithstanding the reputations of these and other scholars asserting such contentions, no one is constrained to accept their arguments uncritically. To do so would be a serious mistake in light of the precisely worded monetary provisions of the Constitution, no scholar with this pessimistic perspective has demonstrated that the Constitution supports his position. The Constitution provides that “The Congress shall have Power”:[60]

To borrow Money on the credit of the United States;[61]

To coin Money, regulate the value thereof, and of foreign Coin;[62] and

To provide for the Punishment of counterfeiting the Securities and current Coin of the United States;[63]

and further, that

No Money shall be drawn from the Treasury, but in Consequence of Appropriations made by Law;[64]

No State shall . . . emit Bills of Credit; [or] make any Thing but gold and silver Coin a Tender in Payment of Debts;[65]

Finally, the Constitution explicitly refers to the dollar as the unit of monetary value.[66]

This silence about the Constitution by people who are otherwise staunch friends of sound money and honest banking is strange. Why, without citing a definitive interpretation of the monetary powers and disabilities of the Constitution, do they assume that the Constitution does not already subject the grant of the government’s power to issue money to rules that limit that power? Indeed, as this article will show, the Founding Fathers did embody in the Constitution the principle that the government should adopt a physical unit of a designated commodity as its monetary unit.

IV. REDISCOVERING THE CONSTITUTIONAL DOLLAR

If the time for constitutional reform is still ripe, the means used for such reform must nevertheless fit for the task. The goal must always be to determine the “original intent” of the supreme law. In the area of monetary and banking law, nothing could be more important than ascertaining that original intent with respect to the noun “dollar,” which appears once in the Constitution proper[67] and once in the Bill of Rights.[68] The Constitution, however, does not define the word “dollar.” So what did that word mean to the Founders?

The first step towards elucidating the true meaning of any of the Constitution’s terms is “to review the background and environment of the period in which that constitutional language was fashioned and adopted,”[69] “to place ourselves as nearly as possible in the condition of the [Framers],”[70] and “to recall the contemporary or then recent history of the controversies on the subject” that still “were fresh in the memories of those who achieved our independence and established our form of government.”[71]

A. English Common Law in the Colonies

Pre-constitutional English common law is one of the most important legal-historical sources of the meaning of many constitutional provisions.[72] Blackstone’s Commentaries[73] was the most satisfactory exposition of the law available to Colonial Americans. “At the time of the adoption of the Federal Constitution, [the Commentaries] had been published about twenty years, and it has been said that more copies of the work had been sold in this country than in England, so that undoubtedly the framers of the Constitution were familiar with it.”[74] Blackstone’s discussion of the English monetary powers was detailed:

Money is an universal medium, or common standard, by comparison with which the value of all merchandise may be ascertained: . . . a sign, which represents the respective values of all commodities. Metals are well calculated for this sign, because they are durable and are capable of many subdivisions: and a precious metal is still better calculated for this purpose, because it is the most portable. A metal is also the most proper for a common measure, because it can easily be reduced to the same standard in all nations: and every particular nation fixes on it it’s own impression, that the weight and standard (wherein consists the intrinsic value) may both be known by inspection only.

The coining of money is in all states the act of the sovereign power; for the reason just mentioned, that it’s value may be known on inspection. And with respect to coinage in general, there are three things to be considered therein; the materials, the impression, and the denomination.

With regard to the materials, sir Edward Coke lays it down, that the money of England must either be of gold or silver; and none other was ever issued by the royal authority till 1672, when copper farthings and half-pence were coined by king Charles the second . . . . But this copper coin is not upon the same footing with the other . . . .

As to the impression, the stamping thereof is the unquestionable prerogative of the crown . . . .

The denomination, or the value for which the coin is to pass current, is likewise in the breast of the king . . . . In order to fix the value, the weight and the fineness of the metal are to be taken into consideration together. When a given weight of gold or silver is of a given fineness, it is then of the true standard, and called . . . sterling metal. And of this . . . sterling metal all the coin of the kingdom must be made, by the statute 25 Edw. III c. 13. So that the king’s prerogative seemeth not to extend to the debasing or enhancing the value of the coin, below or above the sterling value . . . . The king may also, by his proclamation, legitimate foreign coin, and make it current here; declaring at what value it shall be taken in payments. But this . . . ought to be by comparison with the standard of our own coin; otherwise the consent of parliament will be necessary.[75]

Thus, Blackstone elaborated three monetary principles of the common law: First, the precious metals are “most proper” for money, the “universal medium, or common standard.” Second, the “coin of the kingdom” must consist of gold or silver “of the true standard,” in terms of weight and fineness, or, under English common law prior to 1776, the only “money” possible was undebased gold and silver coin. And third, “to fix the value” of domestic or foreign money meant to establish its “intrinsic value” by comparing “the weight and the fineness of the [precious] metal” in a coin with “the true standard, . . . sterling metal.”[76] This procedure precluded “debasing or inhancing the value of the coin, below or above the sterling value.”[77] Specifically, from 1603 through 1816, England followed a bimetallic monetary policy, whereby the law made no change in the character of the silver coinage, but altered the weight and denomination of the gold coinage in order to secure the concurrent circulation of both.[78] As this article will demonstrate, this was also the policy adopted by the Founding Fathers.[79]

The most important early exercise of the power of the Crown in America to legitimate foreign coin, make it current, and declare at what value it shall be taken in payments occurred with the Parliamentary Act of 1707.[80] This Act tabulated the values for each of the foreign coins which commonly passed as payments in America “according to their Weights, and the Assays made of them in our Mint, thereby shewing the just Proportion which each Coin ought to bear to the other,” and then commanded that various foreign coins “stand regulated, according to their Weight and Fineness, according and in Proportion to the Rate before limited and set for the pieces of eight of Sevil, Pillar, and Mexico.”[81] These “pieces of eight” were Spanish silver dollars.[82] This act made the dollar the money of account for all foreign coins in the Colonies.

B. American Money Under the Articles of Confederation

As early as 1776, Congress began to develop a national system of silver and gold coinage on these common law principles, pursuant to what became its explicit power in the Articles of Confederation “of regulating the alloy and value of coin struck by [Congress’s] own authority, or by that of the respective States.”[83] On May 22 of that year, a congressional committee reported on “the value of the several species of gold and silver [coins] current in these colonies, and the proportion they . . . ought to bear to Spanish milled dollars,” in which Continental Currency was payable.[84] Still presuming that “the holders of bills of credit [i.e., the Continental Currency] will be entitled . . . to receive . . . the amount of said bills in Spanish milled dollars, or the value thereof in gold and silver,” on September 2, a committee of Congress recognized:

[T]he value of such dollars is different in proportion as they are more or less worn, and the value of other silver, and of gold coins, . . . when compared with such dollars, is estimated by different rules and proportions in these states, whereby injustice may happen to individuals, to particular states, or to the whole Union . . . , which ought to be prevented by declaring the precise weight and fineness of the s’d Spanish milled dollar . . . now becoming the Money-Unit or common measure of other coins in these states, and by explaining the principles and establishing the rules by which . . . the said common measure shall be applied to other coins in order to estimate their comparative value.[85]

The committee then suggested the “principle” that all silver coins ought to be estimated according to the quantity of fine silver they contain, and all gold coins according to the quantity of fine gold they contain and the proportion which the value of fine gold bears to that of fine silver in the marketplace.[86] By this “rule” the committee established a table of values of various silver and gold coins relative to the Spanish milled dollar.[87]

The next year, a congressional committee further recommended that a mint be established for coining money; that as much gold and silver bullion as can be procured be purchased, and that the bullion be coined into money; and that any person who brought gold and silver to the mint should be able to have it coined on his own account.[88]

In his letter to Congress on January 15, 1782, Robert Morris, Superintendent of the Office of Finance, commented that, “[a]lthough most nations have coined copper, yet that metal is so impure, that it has never been considered as constituting the money standard. This is affixed to the two precious metals, because they alone will admit of having their intrinsic value precisely ascertained.”[89] “Arguments are unnecessary to shew that the scale by which every thing is to be measured ought to be as fixed as the nature of things will permit,” wrote Morris, concluding that “[t]here can be no doubt therefore that our money standard ought to be affixed to silver.”[90] Although Morris personally favored creating an entirely new standard coin, he recognized that “[t]he various coins which have circulated in America, have undergone different changes in their value, so that there is hardly any which can be considered as a general standard, unless it be Spanish dollars.”[91]

In a plan first published on July 24, 1784, Thomas Jefferson strongly concurred that “[t]he Spanish dollar seems to fulfill all conditions” applicable to fixing the unit of money.[92] “Taking into our view all money transactions, great and small,” he ventured, “I question if a common measure, of more convenient size than the dollar, could be proposed.”[93] Equating the unit and the dollar, he wrote:

The unit, or dollar, is a known coin, and the most familiar of all to the minds of people. It is already adopted from south to north; has identified our currency, and therefore happily offers itself as an unit already introduced. Our public debt, our requisitions and their apportionments, have given it actual and long possession of the place of unit.[94]

Yet Jefferson recognized the necessity of certain practical steps to adopt the dollar as the “Money-Unit”: “If we determine that a dollar shall be our unit, we must then say with precision what a dollar is. This coin as struck at different times, of different weight and fineness, is of different values.”[95] This, Jefferson saw as a problem for economic science to solve through objective measurement, not as a matter for politics to dictate according to arbitrary policy.

If the dollars circulating among us be of every date equal, we should examine the quantity of pure metal in each forming an average for our unit. This is a work proper to be committed to the mathematicians as well as merchants and should be decided on actual and accurate experiments.[96]

“The proportion between the value of gold and silver,” he added, “is a mercantile problem altogether.”[97] Given “[t]he quantity of fine silver which shall constitute the unit,” and “the proportion of the value of gold to that of silver,” Jefferson went on, “a table should be formed . . . classing the several foreign coins according to their fineness, declaring the worth . . . in each class, and that they should be lawful tenders at those rates, if not clipped or otherwise diminished.”[98] Concluding, he encouraged Congress

To appoint proper persons to assay and examine, with the utmost accuracy practicable, the Spanish milled dollars of different dates in circulation with us.

To assay and examine in like manner the fineness of all the other coins which may be found in circulation within these states . . . .

To appoint also proper persons to enquire what are the proportions between the values of fine gold and fine silver, at the markets of the several countries with which we are or probably may be connected in commerce; and what would be a proper proportion here, having regard to the average of their values at those markets . . . .

To prepare an ordinance for establishing the unit of money within these states . . . on the . . . principle[:]

That the money-unit of these states shall be equal in value to a Spanish milled dollar, containing so much fine silver as the assay . . . shall shew to be contained on an average in dollars of the several dates in circulation with us.[99]

On May 13, 1785, a committee presented Congress with Propositions Respecting the Coinage of Gold, Silver, and Copper, which referred to a plan proposing that the money unit be one dollar.[100] “In favor of this Plan,” the committee reported, is “that a Dollar, the proposed Unit, has long been in general Use. Its Value is familiar. This accords with the national mode of keeping Accounts.”[101] Later, the report referred to the dollar as the “Money of Account,” thereby equating that term with the term “Money-Unit.”[102] On July 6, 1785, Congress resolved that “the money unit of the United States of America be one dollar”[103] but did not determine the number of grains of fine silver that historically constituted and defined the dollar. Almost another year elapsed until, on April 8, 1786, the Board of Treasury reported to Congress on the establishment of a mint:

Congress by their Act of the 6th July last resolved, that the Money Unit of the United States should be a Dollar, but did not determine what number of grains of Fine Silver should constitute the Dollar.

We have concluded that Congress by their Act aforesaid, intended the common Dollars that are Current in the United States, and we have made our calculations accordingly.

*****

The Money Unit or Dollar will contain three hundred and seventy five grains and sixty four hundredths of a Grain of fine Silver. A Dollar containing this number of Grains of fine Silver, will be worth as much as the New Spanish Dollars.[104]

Shortly thereafter, on August 8, 1787, Congress adopted this standard as the money unit of the United States.[105]

Perhaps not surprisingly, the coinage policy of the Continental Congress perfectly paralleled the traditional common law approach. First, Congress retained the precious metals, silver and gold, as money. Second, it adopted a physical measure of silver, historically fixed in terms of weight and fineness, as the national money unit. Third, it regulated the values of all other coinage by comparing their weights, fineness, and customary market exchange ratios to that of the money unit. And fourth, it acknowledged the propriety of permitting the market to trade freely in gold and silver, and to determine the quantity of money in circulation through the free coinage of those metals. In this manner, Congress recognized the dollar as an absolute constant of weight and fineness of silver, and refrained even from attempting to deflect the purchasing power of money and all monetary exchange ratios from the levels the market set.

C. American Money Under the Constitution: Hamilton’s Proposals

Almost immediately after ratification of the Constitution, Congress and the Executive began work on a national monetary system, under Congress’ power to coin money, regulate the value thereof, and of foreign coin.[106] On January 28, 1791, Secretary of the Treasury Alexander Hamilton presented to Congress his Report on the Subject of a Mint.[107] “A plan for an establishment of this nature,” he wrote, “involves a great variety of considerations intricate, nice, and important.”[108] Indeed, the erection of a mint was essential to the continued integrity of the nation’s coinage:

The dollar originally contemplated in the money transactions of this country [i.e., the silver Spanish milled dollar], by successive diminutions of its weight and fineness [in the Spanish mints], has sustained a depreciation of five per cent., and yet the new dollar has a currency in all payments in place of the old, with scarcely any attention to the difference between them. The operation of this in depreciating the value of property depending upon past contracts, and . . . of all other property, is apparent. Nor can it require argument to prove that a nation ought not to suffer the value of the property of its citizens to fluctuate with the fluctuations of a foreign mint, or to change with the changes in the regulations of a foreign sovereign. This, nevertheless, is the condition of one which, having no coins of its own, adopts with implicit confidence those of other countries.

The unequal values allowed in different parts of the Union to coins of the same intrinsic worth . . . are inconveniences . . . .

It was with great reason, therefore, that the attention of Congress, under the late Confederation, was repeatedly drawn to the establishment of a mint; and it is with equal reason that the subject has been resumed . . . .[109]

To form “a right judgment of what ought to be done,” Hamilton posed several important questions:

1st. What ought to be the nature of the money unit of the United States?

2d. What the proportion between gold and silver, if coins of both metals are to be established?

….

4th. Whether the expense of coinage shall be defrayed by the Government, or out of the material itself?

5th. What shall be the . . . denominations . . . of the coins?

6th. Whether foreign coins shall be permitted to be current or not; if the former, at what rate, and for what period?[110]

1. Bimetallic System

Recognizing that a “pre-requisite to determining with propriety what ought to be the money-unit of the United States” is “to form as accurate an idea as the nature of the case will admit, of what it actually is,” but claiming that “it is not . . . easy to pronounce what is to be considered the unit in the coins,” Hamilton referred to the resolutions of the Continental Congress on the subject, noted that they had resulted in “no formal regulation on the point, (the resolutions of Congress of the July 6, 1785, and August 8, 1786, having never been carried into operation),” and concluded that “usage and practice . . . indicate the dollar as best entitled to that character.”[111] What Hamilton meant by saying the resolutions of the Continental Congress had “never been carried into operation” is unclear. Certainly, Congress had formally resolved that the money unit of the United States be one dollar, and had adopted a dollar containing 375 ⁶⁴⁄₁₀₀ grains of silver as the money unit of the United States.[112] However, no coins of that weight had been minted, and, the resolutions of the Continental Congress were not binding on the Congress seated under aegis of the Constitution.

As to “what kind of dollar ought to be understood; or, in other words, what precise quantity of fine silver,”[113] Hamilton surveyed the various pieces in circulation over the years and recommended that “[t]he actual dollar in common circulation, has . . . a much better claim to be regarded as the actual money unit.”[114] This would have set the intrinsic value of the dollar as “something between 368 and 374 grains of fine silver.”[115]

From this, no debate is possible as to Hamilton’s and, one may infer, everyone else’s understanding that, as of January 1791, the dollar was no abstract concept, but instead a real silver coin. This provides further evidence fixing the meaning of the term in the Constitution.[116]

Hamilton recognized that the suggestions and proceedings in the Continental Congress had for object the annexing of the title of “money unit” emphatically to the silver dollar.[117] Nevertheless, and without adverting to the Constitution’s references to the dollar, he put forward the view that “a preference ought to be given to neither of the metals for the money unit.”[118] His reasoning was opaque:

A resolution of Congress, of the 6th of July, 1785, declares that the money unit of the United States shall be a dollar; and another resolution of the 8th of August, 1786, fixes that dollar at 375 grains and 64 hundredths of a grain of fine silver. The same resolution, however, determines, that there shall be two gold coins, one . . . equal to ten dollars, and the other . . . equal to five dollars; and it is not explained whether either of the two species of coins, of gold or silver, shall have any greater legality in payments than the other. Yet it would seem that a preference in this particular is necessary to execute the idea of attaching the unit exclusively to one kind. If each of them be as valid as the other in payments to any amount, it is not obvious in what effectual sense either of them can be deemed the money unit rather than the other.[119]

Actually, it is obvious: in a traditional bimetallic system, when the free-market exchange ratio diverges significantly from the statutory exchange ratio, the legal value of the “money unit” remains unchanged, but the legal value of the other metal should be regulated up or down to conform the statutory ratio to the market ratio. In a dual monetary system in which no statutory ratio is fixed, but the law treats the free-market ratio as the legal ratio, the legal value of the “money unit” remains unchanged. However, the legal value of the other metal “floats” with the market. In a practical sense, of course, it may not matter which metal is chosen as the “unit” in either system, as long as the choice is clear.

Although Hamilton personally proposed gold as the unit, rather than silver, “if either were to be preferred,” he concluded that it would be

most advisable . . . not to attach the unit exclusively to either of the metals; because this cannot be done effectually, without destroying the office and character of one of them as money and reducing it to the situation of a mere merchandise . . . which would probably be a greater evil than occasional variations in the unit, from the fluctuations in the relative value of the metals; especially if care be taken to regulate the proportion between them with an eye to their average commercial value.[120]

In this he was partially correct: because converting coins into specie is a costly process, the market exchange ratio between the two metals in a bimettalic system can vary within a narrow range without one metal’s driving the other out of circulation.[121] But Hamilton was incorrect to suggest that this economic process depends on whether one or both metals in a bimetallic system retains the formal legal designation of “unit.”

“If, then,” Hamilton went on, “the unit ought not to be attached exclusively to either of the metals, the proportion which ought to subsist between them in the coins becomes . . . of no inconsiderable moment.”[122] Once again, he was mistaken. In a bimetallic system with a fixed statutory exchange ratio, the proportion between the two metals is critical to their concurrent circulation whether one metal, both metals, or neither metal is formally designated the unit.

Hamilton proposed two options: either “[t]o approach as nearly as can be ascertained, the . . . average proportion . . . in . . . the commercial world,” or “[t]o retain that which now exists in the United States.”[123] Because the first alternative required “better materials than are possessed, or than could be obtained without an inconvenient delay,” he recommended the domestic market ratio of “about as 1 to 15.”[124] “There can hardly be a better rule in any country for the legal than the market proportion,” he explained, “if this can be supposed to have been produced by the free and steady course of commercial principles. The presumption in such a case is that each metal finds its true level, according to its intrinsic utility, in the general system of money operations.”[125]

Interestingly, although Hamilton recognized that the market ratio should be the legal ratio, he did not recommend that Congress fix the statutory ratio as the market ratio without declaring what that ratio was. That idea came to the fore, but still not into the coinage acts, only forty years later.[126] Congress’s neglect in this regard doomed the bimetallic system.[127]

2. Free Coinage

Hamilton then turned to the issue of “free coinage,” which he characterized as “one of the nicest questions in the doctrine of money.”[128] Hamilton recommended “defraying the expense of the coinage out of the metals . . . to allow at the mint such a price only for those metals as will admit of profit just sufficient to satisfy the expense of coinage.”[129] In the course of analyzing this issue, Hamilton restated in emphatic terms the traditional policy against monetary debasement:

[R]aising the denomination of the coin [is] a measure which has been disapproved by the wisest men in the nations in which it has been practised, and condemned by the rest of the world. To declare that a less weight of gold or silver shall pass for the same sum, which before represented a greater weight, or to ordain that the same weight shall pass for a greater sum, are things substantially of one nature. The consequence of either of them . . . is to degrade the money unit; obliging creditors to receive less than their just dues, and depreciating property of every kind . . . .[130]

. . . [T]he quantity of gold and silver in the national coins, corresponding with a given sum, cannot be made less than heretofore without disturbing the balance of intrinsic value, and making every acre of land, as well as every bushel of wheat, of less actual worth than in time past . . . .

. . . [A] rise of prices proportioned to the diminution of the intrinsic value of the coins . . . might be looked for in every enlightened commercial country; but, perhaps, in none with greater certainty than in this; because in none are men less liable to be the dupes of sounds; in none has authority so little resource for substituting names for things.

A general revolution in prices . . . could not fail to distract the ideas of the community, and would be apt to breed discontents as well among those who live on the income of their money as among the poorer classes of the people, to whom the necessaries of life would . . . become dearer . . . .

Among the evils attendant on such an operation are these: creditors, both of the public and of individuals would lose a part of their property; public and private credits would receive a wound; the effective revenues of the Government would be diminished. There is scarcely any point, in the economy of national affairs, of greater moment than the uniform preservation of the intrinsic value of the money unit. On this the security and steady value of property essentially depend.[131]

3. Coin Denominations

On the question of the denominations of the coins, Hamilton recommended two equivalent statutory money units based on weight, a gold coin of 24 ¾ grains of fine gold, and a silver coin of 371 ¼ grains of fine silver. “[N]othing better,” he wrote, “can be done . . . than to pursue the track marked out by the resolution [of the Continental Congress] of the 8th of August, 1786.”[132] Specifically, he proposed (among other coins) “[o]ne gold piece, equal in weight and value to ten units, or dollars,” “[o]ne gold piece, equal to a tenth part of the former, and which shall be a unit or dollar,” and “[o]ne silver piece, which shall also be a unit or dollar.”[133] “The chief inducement to the establishment of the small gold piece,” he argued, “is to have a sensible object in that metal, as well as in silver, to express the unit.”[134] He continued,

The [silver] dollar is recommended by its correspondency with the present coin of that name for which it is designed to be a substitute [i.e., the Spanish milled dollar], which will facilitate its ready adoption as such, in the minds of the citizens. . . . Perhaps it might be an improvement to let the dollar have the appellation either of dollar or unit . … In time the unit may succeed to the dollar….

The eagle is not a very expressive or apt appellation for the largest gold piece, but nothing better occurs. The smallest of the two gold coins may be called the dollar or unit, in common with the silver piece with which it coincides. . . .

As it is of consequence to fortify the idea of the identity of the dollar, it may be best to let the form and size of the new one . . . agree with the form and size of the present.[135]

Once again, Hamilton identified the then-existing dollar—the dollar mentioned in the Constitution—with the Spanish milled dollar: “the present coin of that name for which it [i.e., the new United States dollar] is designed to be a substitute.” His apparent hope that the term “dollar” would eventually conflate with or collapse into the term “unit” mirrored his idea that both silver and gold would serve in that capacity simultaneously. However, his Report nowhere explained how, when the free-market exchange ratio between silver and gold changed (as he expected it would), the legal values of the silver and gold units would change. If, for example, silver appreciated as against gold, would an extant silver dollar be valued at more than a dollar; or would an extant “gold dollar” be valued at less? Thus, in this particular context, Hamilton’s idea of two parallel units was, if not incoherent, at least operationally incomplete. Neither did the Report explain how Hamilton’s new unit (of silver or gold) could succeed to the dollar mentioned in the Constitution, unless that unit always maintained the same value as that dollar—in which case the silver unit was the true unit, the gold unit a unit only so long as the free-market exchange ratio between silver and gold remained at the point Hamilton recommended that Congress adopt.

4. Foreign Coins

As to “the currency of foreign coins,” Hamilton recommended the eventual “abolition of this, in proper season, [when] some considerable progress has been made in preparing substitutes for them,” but

foreign coins may be suffered to circulate precisely on their present footing for one year after the mint shall have commenced its operations. The privilege may then be continued for another year to the gold coins of Portugal, England, and France, and to the silver coins of Spain. And these may still be permitted to be current for one year more at the rates allowed to be given for them at the mint; after the expiration of which the circulation of all foreign coins to cease. . . .

It may, nevertheless, be advisable . . . to repose a discretionary authority in the President of the United States, to continue the currency of the Spanish dollar at a value corresponding with the quantity of fine silver contained in it, beyond the period above mentioned for the cessation of the circulation of the foreign coins.[136]

Thus, Hamilton’s Report restated the traditional monetary principles of Anglo-American common law, as Blackstone had recapitulated them, as the Continental Congress had applied them, and as the Federal Convention had embodied them in the Constitution. Congress, Hamilton urged, should adopt silver and gold as the nation’s monetary substances, at an exchange ratio representing the proportionate value between the metals in the domestic free market. Congress should continue on the track marked out under the Articles of Confederation and the Constitution by employing the dollar as the money-unit—a silver dollar derived directly from the Spanish milled dollar, and a new gold coin containing a silver dollar’s worth of that metal. The government should provide free coinage of both silver and gold, should allow for temporary circulation of foreign silver and gold coins, and should preserve the intrinsic value of the coinage. Hamilton’s one innovation was his notion of a “gold dollar” which would also be the unit, along with the (silver) dollar.

Little more than a year later, Congress enacted these traditional principles into law, at the same time rejecting Hamilton’s innovation. The Coinage Act of 1792[137] initiated a new statutory system embodying the common law and constitutional principles Hamilton had re-affirmed in his Report. Congress followed common law tradition by continuing the use of silver, gold, and copper as “Money.”[138] It reiterated the judgment of the Continental Congress and the Constitution that “the money of account of the United States shall be expressed in dollars or units,”[139] and defined the “DOLLARS or UNITS” in terms of weight, as “of the value of a Spanish milled dollar as the same is now current, and to contain three hundred and seventy-one grains and four sixteenth parts of a grain of pure . . . silver.”[140] Recognizing that to adopt Hamilton’s suggestion of a parallel “gold dollar” would cause confusion, Congress created no such coin, instead mandating the coinage of “Eagles,” “each to be of the value of ten dollars or units,”[141] that is, of the weight of the fine gold equivalent in the market-place to 371 ¼ grains of fine silver. Following Hamilton’s recommendation, though, it fixed “the proportional value of gold to silver in all coins which shall by law be current as money within the United States” at “fifteen to one, according to quantity in weight, of pure gold or pure silver.”[142] And it made “all the gold and silver coins . . . issued from the . . . mint . . . a lawful tender in all payments whatsoever, those of full weight according to the respective values . . . [established in the Act], and those of less than full weight at values proportional to their respective weights.”[143] Congress also provided free coinage,[144] and affixed the penalty of death for the crime of debasing the coinage.[145]

This statute is hugely significant in several respects: First, Congress determined, as an historical fact, the meaning of the term “dollar” as used in the Constitution[146]—to wit, “the Spanish milled dollar as the same is now current,” containing 371 ¼ grains of fine silver.[147] This contemporary factual construction of the Constitution fixes its meaning:

We have . . . a construction of the Constitution made by a Congress which was to provide by legislation for the organization of the Government in accord with the Constitution which had just then been adopted, and in which there were, as representatives and senators, a considerable number of those who had been members of the Convention that framed the Constitution and presented it for ratification. It was the Congress that launched the Government. It was the Congress that rounded out the Constitution itself by the proposing of the first ten amendments which had in effect been promised to the people as a consideration for the ratification. It was the Congress in which Mr. Madison, one of the first in the framing of the Constitution, led also in the organization of the Government under it. It was a Congress whose constitutional decisions have always been regarded, as they should be regarded, as of the greatest weight in the interpretation of that fundamental instrument. This construction was followed by the legislative department and the executive department continuously . . . . [A] contemporaneous legislative exposition of the Constitution when the founders of our Government and framers of our Constitution were actively participating in public affairs, acquiesced in for a long term of years, fixes the construction to be given its provisions.[148]

Thereafter, Congress could not change that construction[149] or otherwise alter the constitutional definition of the dollar[150]—and for more than a century it never attempted to do so.

Second, Congress made crystal clear that the unit of the money system is the silver dollar: “DOLLARS or UNITS—each to be of the value of a Spanish milled dollar as the same is now current, and to contain [371 ¼ grains of pure silver]”;[151] and “the money of account of the United States shall be expressed in dollars or units, . . . and . . . all accounts in the public offices and all proceedings in the courts of the United States shall be kept and had in conformity to this regulation.”[152] So, Congress did not create a “gold dollar,” or establish a “gold standard,” as the popular misconception holds. For example, one edition of The Encyclopedia Britannica claims the “dollar . . . was defined in the Coinage Act of 1792 as either 24.75 gr. (troy) of fine gold or 371.25 gr. (troy) of fine silver.”[153] The act did nothing of the kind. It explicitly defined the “dollar” as a fixed weight of silver, and regulate[d] the value of gold coins according to this standard unit and the market exchange ratio between the two metals. Nowhere did the act refer to a gold dollar, only to various gold coins of other names that it valued in dollars: “EAGLES”—each to be of the value of ten dollars or units,”[154] not to be “ten dollars or units.” Some students of monetary law and history have avoided this elementary mistake,[155] including at one time the Supreme Court.[156] But even legal scholars have stumbled badly over it. For example, at the height of the great monetary and constitutional crisis of the 1930s, when lawyers should have been thinking clearly about both subjects, one law review commentator contended that “[o]ur [gold] dollar at its inception was merely a money of account. The distinction is revived by . . . recent legislation”—by which he meant that no gold dollar was coined in 1792 or in 1934.[157] In one sense he was correct: No gold dollar was coined pursuant to the 1792 Act. But in a larger sense, he was woefully mistaken: The 1792 act recognized no gold dollar that might have been (but happened not to be) coined. The only dollar and unit was the silver dollar, which was coined.

The “of the value of“ language proves more than that no gold dollars existed in 1792. It also shows that the United States statutory dollar of 1792 was not the constitutional dollar of 1789, but a new dollar with the value of the historical constitutional dollar: “DOLLARS or UNITS—each to be of the value of a Spanish milled dollar as the same is now current.” Of course, this must have been true because the constitutional dollar had to pre-exist both the Constitution and the 1792 Act. Thus, with respect to the dollar, both the Constitution and the 1792 Act vindicated the economic analysis of Carl Menger, who pointed out that money is not the invention of government, and requires no political authorization for its use.[158]

Third, Congress reiterated the understanding that the legal value of money is no abstraction subject to arbitrary definition, but consists in a coin’s actual weight in precious metal. Silver and gold coins were to be “lawful tender in all payments . . . , those of full weight according to the respective values . . . declared [in the Act], and those of less than full weight at values proportional to their respective weights.”[159] Even the Supreme Court has been able, at one time, to comprehend the significance of this.[160]

Fourth, the provisions defining the dollar and declaring the money of account—that “DOLLARS or UNITS” are “each to be of the value of a Spanish milled dollar as the same is now current, and to contain [371 ¼ grains of pure silver]”;[161] and that “the money of account of the United States is to be expressed dollars or units”[162]—carry with them a heavy historic tradition. Pointing in the correct direction (although otherwise in error) was the theory of the law review commentator quoted above that “[o]ur [gold] dollar at its inception was merely a money of account.”[163] As is generally true of monetary phenomena, historically, a money of account was not an invention of government, but developed from the commercial practice of maintaining accounts in units of money. For centuries, a money of account—often called “imaginary” money, because such a monetary unit was not reified in an actual coin—served as the standard of deferred payments, or as an accounting device. Actual payments, however, were made in various gold or silver coins in circulation at the time.[164] A money of account serves no purpose in a monometallic system; but in a bimetallic system the device can be used to adjust the legal ratio between silver and gold coins to the market exchange ratio between the two metals, by “crying the currency up or down,”—that is, by increasing or decreasing the values of real coins in terms of the money of account. This would maintain parity between the legal exchange rate of gold to silver and the metals’ relative prices in the free market.[165] One of the strengths of the use of a money of account was that a government could dispense with a mint, by giving “currency” to foreign coins—that is, adopting those coins as part of its official money supply by valuing them in terms of the domestic money of account.[166] The main drawback, however, was that changes in the legal exchange rate between gold and silver were not contemporaneous with changes in the free-market exchange rate. A practical solution to this problem would have been to make the legal exchange rate compulsory only in the absence of the parties’ contractual agreement to the contrary. This would have obviated the inherent instability of the bimetallic system.[167] Unfortunately, after the late 1700s, legislators and economists apparently forgot the concept of “imaginary money.”[168]

In the 1792 Act, the “Spanish milled dollar as the same is now current” can be analogized to an imaginary money in the sense that it was the true, historic unit money of account of the monetary system, but was not to be (because it could not be) coined as such by the United States. All United States silver coins would, however, be permanently regulated in value[169] to this money of account at the ratio of 371 ¼ grains of coined silver to the dollar. And all gold coins would be regulated in value at the free-market exchange rate as proclaimed from time to time by Congress. Initially, Congress chose a statutory denomination of gold “EAGLES” in terms of (silver) dollars.[170]

Congress would have been wiser not to have employed a statutory bimetallic ratio at all, and to have set no statutory dollar values on the gold coins at the mint, instead striking them simply as “EAGLES” with a stamped certification of their content of fine gold when at full weight, and letting their values in dollars be set from day to day in the market.[171] If silver and gold are perfect substitutes as money, the exchange ratio parity between them can be arbitrarily fixed; whereas, if they are imperfect substitutes, statutorily fixing the bimetallic ratio is not feasible.[172] Silver and gold would be imperfect substitutes as money if creditors refused to accept one or the other in payment of debts—for example, where creditors found the weight of silver coin disadvantageous compared to the weight of gold coins of the same free-market value, or where creditors foresaw a depreciation in the purchasing power of one metal relative to the other.[173] Thus, the greater the free-market exchange ratio between equivalent weights of silver and gold, the greater the metals’ imperfection as monetary substitutes for each other, and the less likely a fixed bimetallic ratio will work. So, instead of fixing the bimetallic ratio in 1792 (and at other times thereafter), Congress should have simply minted gold EAGLES without any dollar denominations, and allowed their dollar values to be regulated from day to day in the free market.[174] This would have resulted in a system of dual prices—with some goods and services priced in (silver) dollars, and other goods and services prices in EAGLES, in gold, or in “dollars payable in gold” (that is, the weight of coined gold equivalent on that day to the price of the particular good or service stated in silver dollars).[175] In addition, such an approach would have had a great and lasting educational value, by reminding people every day that money is merely a commodity, with no stable purchasing power.[176]

Adopting a statutory scheme more closely modeled on the traditional money of account approach would not have obviated all problems. For instance, rogue public officials intent on cheating the people could still have devalued the coinage by “crying up” the coin (statutorily raising its nominal value) in relation to the money of account.[177] But it would have avoided the problems the country later faced with the bimetallic system, and certainly overall could not have worked out more unfavorably than the present monetary system, in which the dollar is a wholly imaginary concept, reified willy-nilly in silver, gold, base-metallic “sandwich” coins, and legal tender paper currency.[178]

Fifth, the reliance of Congress on a statutorily defined bimetallic system in the 1792 Act was not entirely an unworkable project. True, such a system is clumsy because it requires careful legislative oversight to amend the statutory ratio between silver and gold as the free-market ratio changes in order to maintain concurrent circulation of both metals. Nevertheless, the history of France from 1785 to 1873 proves that, notwithstanding significant changes in the relative production of silver and gold, a bimetallic system can remain stable where the national economy is large in comparison to the world economy, and where people actually use silver and gold as coins for daily transactions and as reserves for bank notes and deposits.[179]

Interestingly, the 1792 Act[180] did not purport to guarantee that silver and gold would in fact exchange in the marketplace at fifteen to one. For example, the statute lacked a provision allowing a person to bring silver (or gold) bullion to the mint to exchange for gold (or silver) coins. To the contrary: The Act explicitly provided that “as soon as the . . . bullion shall have been coined, the person . . . by whom the same shall have been delivered, shall upon demand receive in lieu thereof coins of the same species of bullion which shall have been delivered.”[181] The government’s only representation was that, for the time being (for Congress always retained the power to change the bimetallic ratio), it would accept silver and gold at fifteen to one “in all payments” to it.[182] Moreover, although the 1792 Act mandated that “[a]ll the gold and silver coins . . . shall be a lawful tender in all payments whatsoever,”[183] nothing in that or any other act (until the 1930s) precluded individuals from entering into “gold-clause” or “silver-clause” contracts specifying which of the metals would be their exclusive medium of payment.[184] Indeed, in the post-Civil War Greenback era, the Supreme Court held that such contracts were exempt from the law declaring United States Notes a legal tender,[185] that such contracts had to be valued in terms of specie dollars,[186] and that such contracts were enforceable for their values in specie.[187] No court in the late 1700s and early 1800s would have ruled any differently.

In sum, the Coinage Act of 1792 demonstrates the first Congress’s adherence to the common law and constitutional principles elucidated heretofore. Congress coined American “DOLLARS or UNITS” as Money containing the intrinsic value of silver in a constitutional dollar, (i.e., a Spanish milled dollar as was then current). It coined American EAGLES as Money containing a fixed weight of pure gold and regulated their value in dollars by comparing their intrinsic value in (or weight of) fine gold to the market equivalent of coined silver. It gave both silver and gold coins legal tender character for their intrinsic values in all payments. It opened the mint to free coinage of the precious metals, and it outlawed debasement of the nation’s new Money.

All of this is hardly surprising. For the statesmen who drafted and approved these measures were more than merely conversant with common law principles, the experiences of the Continental Congress, and the monetary provisions of the Constitution. And their handiwork was more than a coincidental embodiment of those principles, experiences, and provisions. Rather, taking into account the vicissitudes of the time, the Coinage Act of 1792 perfectly reflected what the common law and the law under the Articles of Confederation had been before ratification of the Constitution, and what the constitutional law was then and remains today.[188] It definitively interpreted, elaborated, and applied the Constitution with a clearly constitutional character of its own in sections 9 (definition of the dollar), 14 (free coinage of silver and gold), 16 (legal-tender character for silver and gold coins), and 20 (dollar identified as money of account).[189] In particular, Congress’ determination of the proper weight of the dollar—”of the value of a Spanish milled dollar as the same is now current”[190]—remains for all practical purposes today a statement of constitutional law unalterable except by amendment of the Constitution itself. For, at the remove of almost two centuries, it is most probably impossible to revise the conclusion that 371 ¼ grains of fine silver best represents an average of the various Spanish dollars in circulation in the United States in the years immediately preceding 1792.

The Coinage Act of 1792 regulated the value of domestic gold coins as against the (silver) dollar. Hamilton had recommended in his Report that

foreign coins may be suffered to circulate precisely on their present footing for one year after the mint shall have commenced its operations. The privilege may then be continued for another year, to the gold coins of Portugal, England, and France, and to the silver coins of Spain. And these may still be permitted to be current for one year more at the rates allowed to be given for them at the mint; after the expiration of which the circulation of all foreign coins to cease. . . .

It may, nevertheless, be advisable . . . to continue the currency of the Spanish dollar, at a value corresponding with the quantity of fine silver contained in it, beyond the period above mentioned for the cessation of the circulation of the foreign coins.[191]

The 1792 Act, however, did not regulate the value . . . of any foreign coin as part of the money of the United States.

Almost a year after the Coinage Act of 1792, recognizing the need to make various coins of England, France, Portugal, and Spain officially Money, Congress enacted a statute to regulate their values, declaring that these “foreign gold and silver coins shall pass current as money within the United States, and be a legal tender for the payment of all debts and demands, at [specified] rates.”[192] These, however, were no arbitrary rates. For Congress declared that

no foreign coin that may have been, or shall be issued subsequent to [January 1, 1792] shall be a tender . . . until samples thereof have been found, by assay, at the mint of the United States, to be conformable to the respective standards required, and proclamation thereof shall have been made by the President of the United States.[193]

In anticipation of a supply of United States coins, however, Congress provided that “at the expiration of three years next ensuing the time when the coinage . . . shall commence at the mint [created in the Coinage Act of 1792] . . . all foreign . . . coins, except Spanish milled dollars and parts of such dollars shall cease to be a legal tender”;[194] and “all foreign gold and silver coins (except Spanish milled dollars, and parts of such dollars,) which shall be received in payment for monies due to the United States . . . shall, previously to their being issued in circulation, be coined anew, in conformity to the [Coinage Act of 1792].”[195] Thus, once again, Congress recognized the Spanish milled dollar as the money-unit of the country.

Congress continued this policy until 1857.[196] Finally, in that year, Congress declared that “the pieces commonly known as the quarter, eighth, and sixteenth of the Spanish pillar dollar, and of the Mexican dollar, shall be receivable at the treasury of the United States,” but that “the said coins, when so received, shall not again be paid out, or put in circulation, but shall be recoined at the mint.”[197] Additionally, Congress repealed “all former acts authorizing the currency of foreign gold or silver coins, and declaring the same a legal tender in payment for debts.”[198] Thus, for the first time since 1707,[199] the actual Spanish dollar—the original constitutional dollar—ceased to be part of the official circulating medium of the country and became a true money of account (or imaginary money).

The foregoing establishes the original intent of the Constitution with respect to the term dollar and proves two propositions: (1) that the Constitution is a perfectly intelligible document; and (2) that the present régime in Washington has no idea, or no interest in, what the Constitution means in the area of money. Indeed, even without analyzing the devolution of American monetary law since 1792, any careful reader can immediately grasp that the present confusion in the United States Code[200] represents a complete rejection on the part of Congress of the keystone of the Founding Fathers’ monetary structure.

VI. NONCONSTITUTIONAL REFORM

A. Monetary Constitutions