Last Updated on January 15, 2023 by Constitutional Militia

The Federal Reserve System

The Federal Reserve System is a cartel that controls the United States money supply and redistributes wealth with the blessings of the United States Congress. For more details on that particular see The Federal Reserve System: A Fatal Parasite On The American Body Politic

Any State Can Walk Away From the Federal Reserve System: Alternative Constitutional Currency

Model Legislation for Protection Individuals Who Choose to Walk Away From the Federal Reserve System: Monetary Reform 101 and Monetary Reform 102

Individuals using “gold clauses” can, to the extent of those clauses, separate their finances from the Federal Reserve System entirely.

Federal Reserve System: Cartel Structure

In 1913 Congress created the Federal Reserve System (“FRS”).[1] The System’s history, structure, and general activities are well covered in both popular and scholarly literature.[2] The FRS is a quasi central bank, composed of several parts, one (the Board of Governors) arguably public, one (the Federal Open Market Committee) a mixture of public and private elements, and the rest undoubtedly private, with the whole operation organized on a regional basis. Au fond, the System consists of the Board,[3] the Open Market Committee,[4] the Federal Advisory Council,[5] twelve Federal Reserve Regional Banks,[6] and thousands of privately owned “member banks” located throughout the United States[7] The FRS’s function is to control the availability and cost of bank reserves, bank credit, and paper currency (Federal Reserve Notes, or “FRNs”). It conducts this “monetary policy”—that is, redistribution of wealth through manipulation of media exchange—in three ways:[8] By engaging in “open market operations”—the purchase and sale primarily of government securities to control the amount of reserves in the banking system. By regulating “reserve requirements”—the money member banks and other depository institutions must hold against their deposits. And by manipulating the “discount rate”—the interest a Federal Reserve regional bank charges member banks and depository institutions for its loans.

According to the Board of Governors, “[t]he entire System is subject to oversight by the U.S. Congress because the Constitution gives Congress the power to coin money and set its value—a power that the 1913 Act, Congress itself delegated to the Federal Reserve”.[9] But one can search that Act until his eyes fall out without finding a single delegation of “the power to coin money”. The closest approximation resides in Section 16 of the Act, which provided that

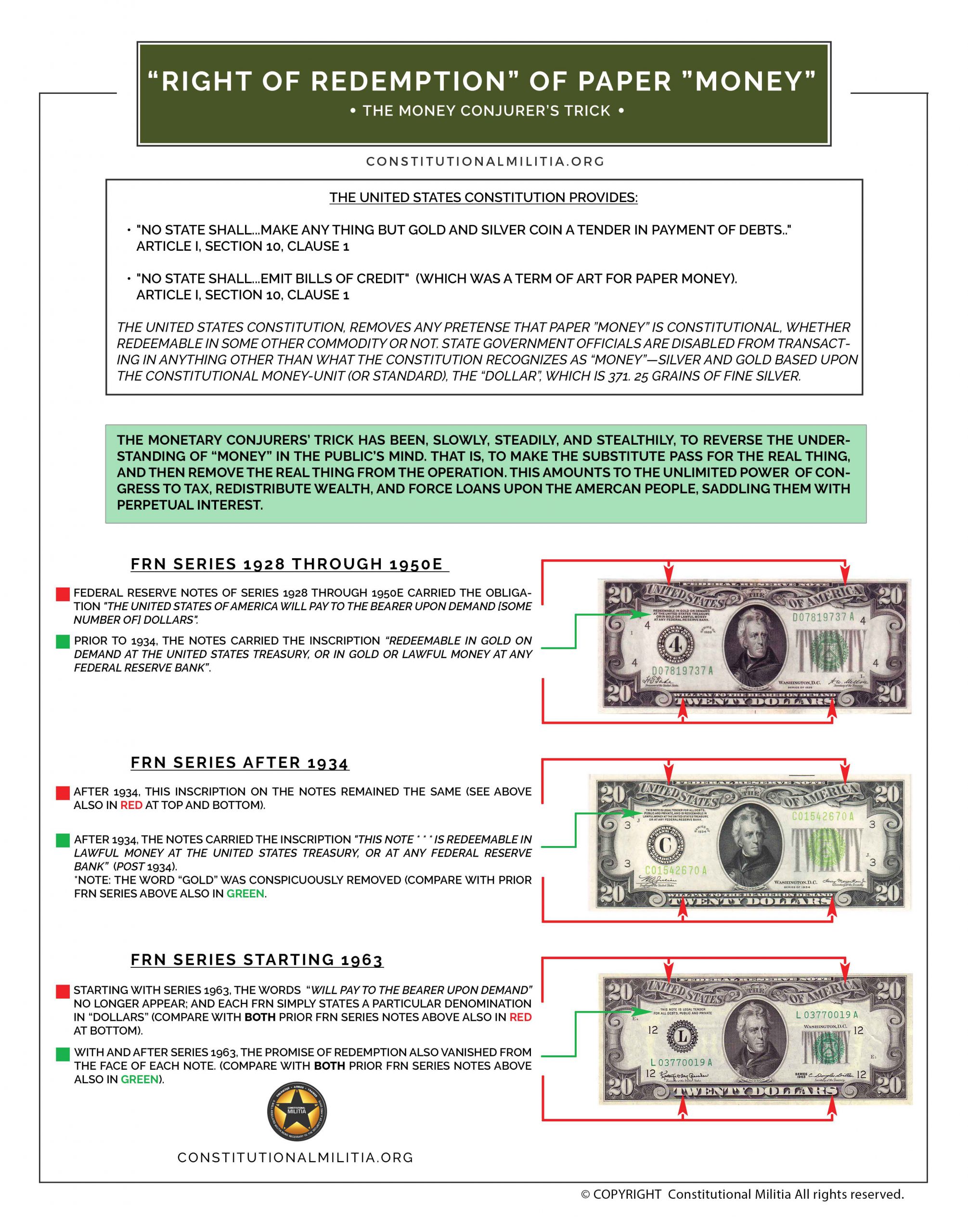

Federal reserve notes, to be issued at the discretion of the Federal Reserve Board for the purpose of making advances to the Federal reserve banks * * * and for no other purpose, are hereby authorized. The said notes shall be obligations of the United States and shall be receivable by all national and member banks and Federal Reserve banks and for all taxes, customs and other public dues. They shall be redeemed in gold on demand at the Treasury Department of the United States * * *, or in gold or lawful money at any Federal reserve bank.[10]

As amended by the Gold Reserve Act of 1934, which struck the requirement for redemption in gold,[11] the present codification of Section 16 provides that “[t]hey [i.e., FRNs] shall be redeemed in lawful money on demand at the Treasury * * * or at any Federal Reserve bank”,[12] which redemption does not include exchanges of paper currency for gold or silver coin.[13] Inasmuch as this provision licenses the Board only to “issu[e]” notes “redeem[able] in lawful money”, and inasmuch as no statute has ever declared FRNs themselves to be “lawful money”, the Board cannot even be “issu[ing]” such “money” when it causes FRNs to be printed by the Treasury,[14] let alone “coin[ing]” it.

The Board’s hyperbolic claim does illustrate, however, how the “living” Constitution evolves, even outside of courtrooms. The Supreme Court has never held, or even intimated, that Congress has delegated its constitutional power “To coin Money”[15] to the Board or to the FRNs on the System’s behalf. Indeed, such a holding would be rather extraordinary, inasmuch as in Knox v. Lee[16] Justice Strong’s opinion for the court “d[id] not rest the [ ] validity [of the Treasury’s emission of legal-tender paper currency] upon the assertion that [such] emission is coinage, or any regulation of the value of money”, and did not “assert that Congress may make anything which has no value money”;[17] and Justice Bradley’s decisive concurring opinion held that the supposed Congressional power to issue paper currency “is entirely distinct from that of coining money and regulating the value thereof”.[18] Nevertheless, the Board of Governors simply arrogates to itself a purportedly delegated Congressional power that, besides being self-contradictory on its face (to emit paper currency irredeemable in silver or gold coin under color of the power “To coin”), according to the Supreme Court Congress itself does not enjoy. To be sure, if pressed the Board could always fall back on the rationalization that Congress has really delegated it to it the authority to “issue[ ]” FRNs under color of the power “To borrow Money”,[19] which Justice Bradley in Knox identified as a source of Congress’s supposed authority to “emit bills”,[20] Revealingly, though, Bradley considered the emission of the Greenbacks as constituting a forced loan, supposedly justified by the emergency of the Civil War.[21] On what theory Congress could impose a forced loan on Americans in peacetime no one has ever explained. Moreover, the Supreme Court has never held that Congress may delegate to a governmental agency (if the Board is one), let alone to private banks brigaded in a cartel, a license to impose forced loans on Americans through the emission of “bills” under color of the Congressional power “To borrow Money”. So, the Board’s claim is, not only hyperbolic , but also without plausible basis in even the Supreme Court’s mythological misconstruction of the latter power.[22]

The international political and financial crime families know full well that the Federal Reserve System—indeed, the whole complex, corrupt apparatus that couples private banks and public institutions through the Treasury of the United States—is inherently unstable and needs to be replaced, because it can no longer be propped up, let alone reformed in any fundamental sense. Aware that the Federal Reserve System’s days are numbered, they intend to translate the paper-currency scam to the next level, just as they have done, step by step, in crisis after crisis, throughout American history.[23]

{kind=link}