Last Updated on February 19, 2023 by Constitutional Militia

“What Is A “Dollar”?

AN HISTORICAL ANALYSIS OF THE FUNDAMENTAL QUESTION IN MONETARY POLICY

National Alliance for Constitutional Money

Monograph No. 6

by Edwin Vieira, Jr.

Foreword

Today, all thinking, informed Americans know their country is in trouble. Many haven’t a clue as to what went wrong with their government, while others can recite a litany of reasons for their country’s distress. Of course, no one reason is paramount; but surely a debased, corrupt, and inflationary monetary system must be placed near the top of the list of causes of America’s woes.

What To Do About It?

This Monograph presents, in irrefutable fashion, the legal and economic history of the “dollar,” and of the “dollar’s” role in America’s monetary system, as originally devised by the Founding Fathers. It also analyzes the Coinage Act of 1792, signed into law by President Washington, which put into effect the monetary system the Founders had previously outlined in the Constitution.

This system helped make the United States “dollar” the safest, most sought-after currency in the world, leading to the well-known saying “sound as a dollar.” However, in 1913, Congress—in an unconstitutional act—relinquished its constitutional power and duty to “coin Money and regulate the Value thereof” to a private banking cartel, the Federal Reserve System.

The ensuing years witnessed a gradual abandonment of the Founding Fathers’ system (based on silver and gold coins) and the insidious substitution of a paper-currency system based on irredeemable, fiat Federal Reserve Notes, which continue to circulate today only because of the public’s misplaced confidence.

What to do about it? is the question. Obviously, the Federal Reserve System’s experiment with fiat currency has failed. But we cannot have a sound economy without sound money. That means we must return to a monetary system based on silver and gold coins—as the Founding Fathers wisely specified. This will require action by Congress to rectify its mistake of 1913, by abolishing the Federal Reserve System and reaffirming the “dollar” as a coin containing 371.25 grains (troy) of fine silver.

We know that Congress will take no such action on its own initiative. Congress will move only when the general public becomes aware of, and incensed by, the monetary mess Congress and the Federal Reserve System have created. Therefore, everyone concerned with “the money issue” must bring the facts to the attention of as many Americans as possible.

This Monograph contains more than enough documentation to convince anyone of good faith and an open mind of what a “dollar” is. This documentation should be used in every possible way to generate public debate on the money issue: letters to the editor, call-ins to radio talk shows, local citizens’ meetings, and so on. All these offer opportunities to present powerful arguments for a restoration of the constitutional monetary system, and to wrest the initiative in the public forum away from the Federal Reserve System and its apologists.

As the Monograph concludes, “modern money has become a means for the total confiscation of private property by the government.” It is, therefore, incumbent on those of us who understand this issue to make the truth known to others. Nothing could be more vital than to restore the monetary system with a proven track record: the one devised by our Founding Fathers!

Richard L. Solyom, Chairman

Sound Dollar Committee

Introduction

The question “What is a ‘dollar’?” may seem trivial. Everyone knows what a “dollar” is—or, at least almost everyone thinks he does. In fact, however, very few people could correctly define a “dollar.” And even fewer know why a correct definition is vital to their continued economic and political well-being.

Analysis

1. Why is a correct definition of the term “dollar” important?

The United States has a highly advanced free-market economy. In a free-market economy, the prices of almost all goods and services are stated in units of money. Under present law—and, as will be described below, from the very beginnings of this country—”United States money is expressed in dollars * * * .”[1] Moreover, all “United States coins and currency (including Federal Reserve Notes * * *) are legal tender for all debts, public charges, taxes and dues.”[2] Thus, all “coins and currency (including Federal Reserve notes * * * )” that are “expressed in dollars” are both money and legal tender. For this reason, accurately defining the noun “dollar” is mandatory, in order to know what is supposedly the official “Money” of the United States and what constitutes “legal tender for all debts, public charges. taxes and dues.”[3]

2. Do the present monetary statutes intelligibly define the “dollar'”?

Unfortunately, the present monetary statutes do not define the “dollar” in an intelligible fashion.

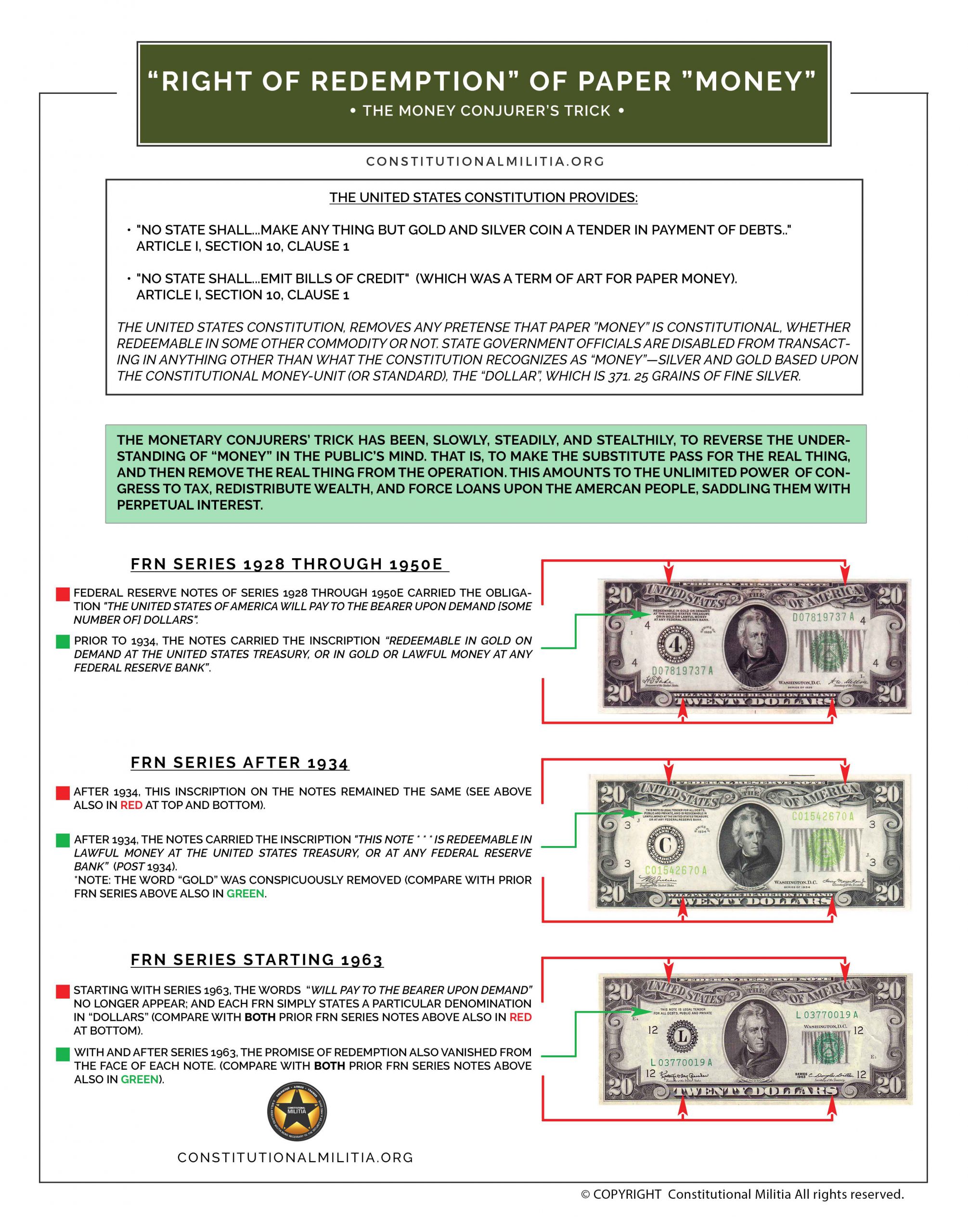

a. Federal Reserve Notes. Most people associate the noun “dollar” with the Federal Reserve Note (“FRN”) “dollar bill,” engraved with the portrait of President George Washington. This association is mistaken.

No statute defines—or ever has defined—the “one dollar” FRN as the “dollar,” or even as a species of “dollar.” Moreover, the United States Code provides that FRNs “shall be redeemed in lawful money on demand at the Treasury Department of the United States * * * or at any Federal Reserve bank.”[4] Thus, FRNs are not themselves “lawful money”—otherwise, they would not be “redeemable in lawful money.” And if FRNs are not even “lawful money,” it is inconceivable that they are somehow “dollars,” the very units in which all “United States money is expressed.”[5]

People are confused on this point because of the insidious manner in which FRNs “evolved”—actually, degenerated is a more appropriate verb—from the late 1920s until today. FRNs of Series 1928 through Series 1950E carried the obligation “The United States of America will pay to the bearer on demand [some number of] dollars.” Prior to 1934, the notes carried the inscription “Redeemable in gold on demand at the United States Treasury, or in gold or lawful money at any Federal Reserve Bank.” After 1934, the notes carried the inscription “this note * * * is redeemable in lawful money at the United States Treasury, or at any Federal Reserve Bank” (post-1934). Starting with Series 1963, the words “will pay to the bearer on demand” no longer appear; and each FRN simply states a particular denomination in “dollars.”

With and after Series 1963, the promise of redemption also vanished from the face of each note.[6] Thus, on their faces FRNs became, in the apt description of banking expert John Exter, an “I.O.U. Nothing” currency. This change in the mere language printed on FRNs could not transform their legal character, however. If FRNs were not “dollars” when they explicitly promised to pay in gold or “lawful money,” they did not magically become “dollars” when they stopped explicitly promising to pay in anything at all.[7]

b. United States coins. The situation with coinage is more complex, but equally (if not more) confusing. The United States Code provides for three different types of coinage denominated in “dollars”: namely, base-metallic coinage, gold coinage, and silver coinage.

(1) The base-metallic coinage consists of “a dollar coin,” weighing “8.1 grams,” “a half dollar coin,” weighing “11.34 grams”; “a quarter coin,” weighing “5.67 grams”: and “a dime coin,” weighing “2.268 grams.”[8] All of these coins are composed of copper and nickel.[9] The weights of the dime, the quarter, and the half dollar are in the correct arithmetical proportions, the one to each of the others.[10] But the “dollar” is disproportionately light (or the other coins disproportionately heavy). In this series of base metallic coins, then, the questions naturally arise: Is the “dollar” a cupro-nickel coin weighing “8.1 grams”? Or is it two cupro-nickel coins (or four or ten coins) collectively weighing 22.68 grams? Or is it both? Or is it neither, but something else altogether, to which the weights of these coins are irrelevant?

(2) Similarly, the gold coinage consists of “[a] fifty dollar gold coin” that “weighs 33.931 grams, and contains one troy ounce of fine gold”; “[a] twenty-five dollar gold coin” that “contains one-half ounce of fine gold”; “[a] ten dollar gold coin” that “contains one fourth ounce of fine gold”; and “[a] five dollar gold coin” that “contains one tenth ounce of fine gold.”[11] The “fifty dollar,” “twenty-five dollar,” and “five dollar” coins are in the correct arithmetical proportions each to the others. But the “ten dollar” coin is not. Therefore, is a “dollar” one-fiftieth or one-fortieth of an ounce of gold? Or both? Or neither?

And what is the logical, economic, or other relationship between a “dollar” that contains “8.1 grams” of copper and nickel, and a “dollar” that consists of 0.679 grams of gold alloy?[12]

(3) Finally, the silver coinage consists of a coin that is inscribed “One Dollar,” weighs “31.103 grams,” and is supposed to contain one ounce of .”999 fine silver.”[13]

What is the rational relationship between this “dollar” of “31.103 grams” of “.999 fine silver,” a “dollar” containing 0.679 grams of gold alloy, and a “dollar” containing “8.1 grams” of base metals? Obviously, these are not the amounts of the metals that exchange against each other in the free market—that is, the different weights of different metals do not reflect equivalent purchasing powers. So, on what theory are each of these disparate weights, and purchasing powers, equally “dollars”?

c. Currency of “equal purchasing power” The United States Code provides no answer to this perplexing question. Indeed, it mandates that the question should not even be capable of being asked. For the Code commands that “the Secretary [of the Treasury] shall redeem gold certificates owned by the Federal reserve banks at times and in amounts the Secretary decides are necessary to maintain the equal purchasing power of each kind of United States currency.[14]

One need be no expert in currency transactions to know that a “fifty-dollar” gold coin has significantly more purchasing power than a “fifty-dollar” FRN or than fifty cupro-nickel “dollars,” and that a “one-dollar” silver coin has significantly more purchasing power than a “one-dollar” FRN or one cupro-nickel “dollar.” Thus, one need be no expert in administrative law to realize that the Secretary of the Treasury has defaulted on his obligation to keep all forms of “United States currency” at parity with each other—that is, to maintain a “dollar” of the same purchasing-power, whether it be composed of gold, silver, or base metals.

The Secretary’s default cannot be traced to a lack of power to perform his duty. For example,

“With the approval of the President, the Secretary of the Treasury may

– (A) buy and sell gold in the way, in amounts, at rates, and on conditions the Secretary considers most advantageous to the public interest; and (B) buy the gold with any direct obligations of the United States Government or United States coins and currency authorized by law * * *.”[15]

“The Secretary may buy silver mined from natural deposits in the United States that is brought to a United States mint or assay office within one year after the month in which the ore from which it is derived was mined.”[16]

“The Secretary may sell or use Government silver to mint coins * * * . The Secretary shall sell silver under conditions the Secretary considers appropriate for at least $1.292929292 a fine troy ounce.”[17] “Except to the extent authorized in regulations the Secretary of the Treasury prescribes with the approval of the President, the Secretary may not redeem United States currency (including Federal reserve notes * * *) in gold. * * * When redemption in gold is authorized, the redemption may be made only in gold bullion bearing the stamp of a United States mint or assay office in an amount equal at the time of redemption to the currency presented for redemption.”[18]

Thus, the United States Code simply presents another unanswered question: “Why has the Secretary of the Treasury failed ‘to maintain the equal purchasing power of each kind of United States currency’?”

In sum, the present monetary statutes of the United States do not define the noun “dollar” in an unique way. Instead of monetary law—which, by hypothesis, requires clearly defined terms and rational relationships among those terms—the country’s present monetary code smacks of political psychosis—in which completely different things have the same name, things unequal to each other are treated as equivalent, and things that should have the same characteristics (e.g., “equal purchasing power[s]”) are quite different.

3. What do American history and the Constitution identify as the “dollar”?

Reference to history clears away the confusion of present-day politics, by showing beyond cavil that the “dollar” is a specific coin, containing 371.25 grains (troy) of fine silver, and nothing else.

a. The “dollar” in the Constitution. Both Article 1, Section 9, Clause 1 and the Seventh Amendment to the Constitution refer explicitly to the “dollar”—in the one case, permitting “a Tax or duty * * * not exceeding ten dollars for each Person” the States saw fit “to admit” prior to 1808; and, in the other, guaranteeing trial by jury ” [i]n suits at common law, where the value in controversy shall exceed twenty dollars.” The Constitution does not define this “dollar.” But, in the late 1700s, no explicit definition was necessary: Everyone conversant with political and economic affairs knew that the word imported the silver Spanish milled dollar.

Indeed, had not such an understanding been catholic, powerful contending forces might never have agreed to support the Constitution at all. For example, the traditional interpretation of Article 1, Section 9, Clause 1 is that it elliptically refers to the slave-trade, and represents a compromise between pro- and anti-slavery forces that was vital to ratification of the Constitution.[19] Self-evidently, those in the pro-slavery faction would never have accepted the “Tax or duty” phrase unless they already knew that the “dollar” identified as the measure of the “Tax” had a fixed value, and what its value was. Otherwise, by monetary manipulation aimed at increasing the purchasing-power of the “dollar,” anti-slavery forces in Congress might have eliminated the slave-trade altogether.

Similarly, the proponents of the fundamental right to jury-trial in the Seventh Amendment would never have accepted the “dollar”-limitation on jury-trials unless they already knew that the “dollar” had a fixed value, and what its value was. Otherwise, monetary manipulation might have eliminated common-law juries altogether. Yet both these groups also were aware of the doctrine that, if Congress had discretion to change the value of the unit of money, there could be no legal limits to the changes it might make.[20] Therefore, their support of these provisions inferentially establishes what a literal reading of them straightforwardly suggests: to wit, that the noun “dollar” refers, not to a mere name applicable to whatever Congress whimsically might decide thereafter to call a “dollar,” but instead to a particular coin so familiar in American experience as to be beyond political transmogrification.

An interpretation of the term “dollar” as signifying merely the label the Constitution gives to whatever Congress decides to make the unit of money, if consistently applied to other undefined terms in the document, would render the Constitution nonsensical. For example, the noun “Year” appears repetitively in Article I—particularly in Section 2, Clause 1 (“The House of Representatives shall be composed of Members chosen every second Year”), and Section 3, Clause I (“The Senate of the United States shall be composed of two Senators from each State, chosen by the Legislature thereof, for six Years”).

Self-evidently, the Framers used this term with the presumption that everyone would implicitly understand it to mean the time the earth actually requires for one complete revolution around the sun—rather than a mere empty shorthand for a unit of time within the discretion of Congress to adopt or change. Yet, if the word “dollar” need have no fixed, historically ascertainable meaning, neither need the word “Year.” The principle of constitutional interpretation is precisely the same in both cases. And if the noun “Year” need have no meaning more fixed than the noun “dollar” does in present-day monetary statutes (as discussed above), then Congress could enact laws “redefining” the “Year” so as to extend, for instance, the terms of the House and Senate to ten, twenty, one hundred, or any other number of earthly revolutions.

Of course, Congress may, with constitutional propriety, appoint astronomers, physicists, and other qualified experts to determine with scientific precision what the “Year” actually is. Congress lacks authority, however, to decide for itself what the “Year” ought to be, or to declare the “Year” to be whatever Congress may arbitrarily desire from time to time. Analogously, Congress may, with constitutional propriety, appoint economists, monetary historians, and other experts to determine with clinometric accuracy what the “dollar” actually was in the late 1700s. In fact, this is what Congress did do, under both the Articles of Confederation and the Constitution (as described below). Congress has no authority, however, to decide for itself what the “dollar” ought to be.

Besides constitutional history and logic, economic analysis and history support an interpretation of the noun “dollar” as referring to a specific thing the character of which was an ascertainable historical fact that Congress was obliged to determine, rather than as constituting merely a political label that Congress could assign to whatever it deemed expedient. The nominalistic view that would treat the term “dollar” as simply a convenient, historically vacuous term for whatever Congress chooses to declare to be “money,” and set up as the “unit of value,” is incapable of answering the question: “What is an abstract ‘unit of value’?,” and passes over in silence the question: “Before ratification of the Constitution, was the ‘dollar’ something that it ceased to be thereafter?”

Economically, of course, “abstract” (or “objective”) value does not exist, in monetary matters or elsewhere. In general, the notion that value is objective is “[a]n inveterate fallacy”; and the allied concept that value is measurable in terms of some definedly fixed unit is a “spurious idea.” Simply put, “[t]here is no method available to construct a unit of value.” More specifically, “money is not a standard for the measurement of prices; it is a medium whose exchange ratio varies in the same way * * * in which the mutual exchange ratios of the vendible commodities and services vary.” Furthermore, money can never arise ex nihilo. “The acceptance of anew kind of money presupposes that the thing in question already has, previous exchange value on account of the services it can render directly to consumption or production.”[21] In short, no governmental edict can make something with no previously existing purchasing power either a “unit of value,” or “money” in the economic sense.

Prior to ratification of the Constitution, no one conversant with economics and commercial practices conceived of monetary values as abstractions. Rather, “money” was generally synonymous with known weights of the precious metals, gold and silver, and (to a lesser degree) the base metals, such as copper. In particular, Anglo-American monetary history records that merchants traditionally tendered and accepted coins, the standard monetary instruments of the times, not by tale without consideration of those coins’ qualities. but only as pieces of precious metal of specific weights and fineness.

Where commercial practice accepted payment of coins by tale, it was always with the definite belief that those coins’ stamps assured them to be of the correct weights and usual fineness for their types. Absent grounds supporting this assumption, merchants regularly resorted to weighing and chemical analyses. Thus, commercial practice always insisted that the “value” of coins was not their face-values as abstract governmental tokens, but only their market-values as pieces of actual metal. And whenever circumstances indicated that a stamp no longer reflected a coin’s physical content, merchants ceased relying on the official monetary “value,” and substituted their own system for measuring the coin’s market-worth in precious metal.

From an early day, the law applicable to America conformed to this age-old commercial understanding. Queen Anne’s Proclamation of 1704, for example, spoke not of abstract values, but of “the value of * * * coins which usually pass in payment in our said plantations [in America], according to their weight, and the assays made of them in our mint,” and specifically referred to the “Sevil, Pillar, or Mexico pieces of eight” (various forms of Spanish silver dollars) as having “the full weight of seventeen penny-weight and an half”—thereby recognizing that the value” of a coin lay in its “weight” and “assay” according to a fixed standard, or “full weight.”[22]

Thus, at the time of ratification of the Constitution, no person with any understanding of law and monetary affairs would have attributed to the noun “dollar” a meaning other than (for example): “a silver coin with a value of such-and-so grains of precious metal when at full weight.”[23]

b. Adoption of the “dollar” as the unit of money prior to ratification of the Constitution. The actions of the Continental Congress itself prove that the foregoing analysis is correct.

The Founding Fathers did not need explicitly to adopt the “dollar” as the national unit of money or to define that noun in the Constitution—because the Continental Congress had already performed that task.

I. Use of the dollar as a standard coin and monetary unit did not begin with the Continental Congress, however. Monetary historians generally first associate the dollar with one Count Schlick, who began striking such silver coins in 1519 in Joachim’s Thai, Bavaria. Then called “Schlickten thalers” or “Joachimsthalers,” the coins became known simply as “thalers,” which transliterated into “dollars.” Interestingly, the American Colonies did not adopt the dollar from England, but from Spain. Under that country’s monetary reforms of 1497, the silver real became the Spanish money-unit, or unit of account. A new coin consisting of eight reales also appeared.

Variously known as pesos, duros, piezas de a ocho (“pieces of eight”), or Spanish dollars (because of their similarity in weight and fineness to the thaler), the coins quickly achieved predominance in financial markets of the New World because of Spain’s then-important commercial and political position.[24] Indeed, by 1704, the “pieces of eight” had in fact become a unit of account of the Colonies, as Queen Anne’s Proclamation of 1704 recognized, when it decreed that all other current foreign silver coins “stand regulated, according to their weight and fineness, according and in proportion to the rate before limited and set for the pieces of eight of Sevil, Pillar, and Mexico.”[25]

By the War of Independence, the Spanish dollar was, for all practical purposes, rapidly becoming the monetary unit of the American people as a matter of economics. Not surprisingly, the Continental Congress first used, and then took formal steps to adopt, that dollar as the nation’s standard of value. On 22 May 1776, a Congressional committee reported on “the value of the several species of gold and silver coins current in these colonies, and the proportions they ought to bear to Spanish milled dollars.” And on 2 September of that year, a further committee-report undertook to “declar[e] the precise weight and fineness of the * * * Spanish milled dollar * * * now becoming the Money-Unit or common measure of other coins in these states and to “explai[n] the principles and establish the rules by which * * * the said common measure shall be applied to other coins * * * in order to estimate their comparative values.”[26]

Meanwhile, Congress and its agents were carefully exploring the basis of, and possible structures for, a national monetary-system. In his letter to Congress of 15 January 1782, Robert Morris, Superintendent of the Office of Finance, commented that, ” [a]lthough most nations have coined copper, yet that metal is so impure, that it has never been considered as constituting the money standard. This is affixed to the two precious metals [i.e., silver and gold], because they alone will admit of having their intrinsic value precisely ascertained.” “Arguments are unnecessary to shew that the scale by which every thing is to be measured ought to be as fixed as the nature of things will permit,” wrote Morris, concluding that”[t]here can be no doubt therefore that our money standard ought to be affixed to silver.” Although Morris personally favored creating an entirely new standard coin, he recognized that “[t]he various coins which have circulated in America, have undergone different changes in their value, so that there is hardly any which can be considered as a general standard, unless it be Spanish dollars.”[27]

In a plan first published on 24 July 1784, Thomas Jefferson strongly concurred that ” [t]he Spanish dollar seems to fulfill all * * * conditions” applicable to “fixing the unit of money.” “Taking into our view all money transactions, great and small,” he ventured, “I question if a common measure, of more convenient size than the dollar, could be proposed.” “The unit, or dollar,” he wrote equating the one with the other, “is a known coin, and the most familiar of all to the minds of people. It is already adopted from south to north: has identified our currency, and therefore happily offers itself as an unit already introduced. Our public debt, our requisitions and their apportionments, have given it actual and long possession of the place of unit.”[28]

Yet Jefferson recognized the necessity of certain practical steps to adopt the dollar as the “Money-Unit”: “If we determine that a dollar shall be our unit, we must then say with precision what a dollar is. This coin as struck at different times, of different weight and fineness, is of different values.” This, though, Jefferson saw as a problem for economic science to solve through objective measurement, not as a matter for politics to dictate according to arbitrary policy. “If the dollars circulating among us be of every date equal, we should examine the quantity of pure metal in each, and from them form an average for our unit. This is a work proper to be committed to the mathematicians as well as merchants, and which should be decided on actual and accurate experiments.” “The proportion between the value of gold and silver,” he added, “is a mercantile problem altogether.” Given “[t]he quantity of fine silver which shall constitute the unit,” and “the proportion of the value of gold to that of silver,” Jefferson went on, “a table should be formed * * * classing the several foreign coins according to their fineness, declaring the worth * * * in each class, and that they should be lawful tenders at those rates, if not clipped or otherwise diminished.”[29]

Concluding, he encouraged Congress:

To appoint proper persons to assay and examine, with the utmost accuracy practicable, the Spanish milled dollars of different dates in circulation with us.

To assay and examine in like manner the fineness of all the other coins which may be found in circulation within these states.

To appoint also proper persons to enquire what are the proportions between the values in fine gold and fine silver, at the markets of the several countries with which we are or probably may be connected in commerce; and what would be a proper proportion here, having regard to the average of their values at those markets * * * .

To prepare an ordinance for establishing the unit of money within these states * * * on the * * * principle[:]

That the money-unit of these states shall be equal in value to Spanish milled dollar, containing so much fine silver as the assay * * * shall shew to be contained on an average in dollars of the several dates in circulation with us.[30]

Jefferson’s cogent and straightforward analysis of the problem of selecting and defining a unit of money should be compared—contrasted, really—with the present mishmash of monetary statutes that leave the definition of the “dollar” in a state of hopeless confusion today.

First, for Jefferson, the “unit” was to be “a known coin” that was “familiar” to the people because it was “already adopted” in the marketplace. None of the coins that Congress now authorizes—be it of silver, gold, or base metals—was (before its authorization) a “known coin” “familiar” to anyone in the United States, even in terms of its content of metal.

Second, having settled on the “dollar” as the “unit,” for Jefferson the problem of fixing the standard “unit” reduced to determining “what a dollar is” in terms of “the quantity of pure metal” [i.e., silver] contained in “an average” coin that actually circulated in the marketplace. Thus, for Jefferson it was not the prerogative of Congress to create the “dollar” ex nihilo, but the responsibility of Congress to determine what the “dollar” in common use among the people actually was. Today’s Congress assumes that it may declare anything a “dollar,” and then impose that ersatz, political pseudo—”dollar” on the people whether they want it or not.

Third, for Jefferson, to settle the relative values of silver and gold coins was also a matter of studying actual economic relationships in the marketplace: to wit, “the proportion of the value of gold to that of silver” in the various coins in circulation. For today’s Congress, economic relationships between silver and gold are irrelevant. And, of course, there is no rational economic relationship between the coins of base metals and the coins of precious metals, either. Moreover, even within the sets of gold and base-metallic coins themselves, rational economic relationships are irrelevant to Congress!

Obviously, Jefferson’s free-market, scientific approach is a world apart from the arbitrary way in which Congress has set up the mutually incompatible and internally irrational sets of silver, gold, and base-metallic coins that exist today.

On 13 May 1785, a committee presented Congress with “Propositions Respecting the Coinage of Gold, Silver, and Copper,” which referred to the “Plan which proposes that the Money Unit be One Dollar.” “In favor of this Plan,” the committee reported, is “that a Dollar, the proposed Unit, has long been in general Use. Its Value is familiar. This accords with the national mode of keeping Accounts.” Later, the report referred to the “dollar” as the “Money of Account,” thereby equating that term with the term “Money-Unit.”[31]

On 6 July 1785, Congress unanimously “Resolved, That the money unit of the United States be one dollar.”[32] Almost another year elapsed until, on 8 April 1786, the Board of Treasury reported to Congress on the establishment of a mint:

Congress by their Act of the 6th July last resolved, that the Money Unit of the United States should be a Dollar, but did not determine what number of grains of Fine Silver should constitute the Dollar. We have concluded that Congress by their Act aforesaid, intended the common Dollars that are Current in the United States, and we have made our calculations accordingly.

* * * * *

The Money Unit or Dollar will contain three hundred and seventy five grains and sixty four hundredths of a Grain of fine Silver. A Dollar containing this number of Grains of fine Silver, will be worth as much as the New Spanish Dollars.[33]

Shortly thereafter, on 8 August 1787, Congress adopted this standard as “the money Unit of the United States.[34]

Again, stark and striking is the contrast between how the committee of the Continental Congress—composed of the Founding Fathers—approached the problem of fixing the unit of money, and how the modern Congress deals with the same matter. The committee determined that an American”dollar” should contain a known, unchangeable weight of silver, and would be “worth as much as the New Spanish Dollars” because it actually contained this weight of precious metal, not simply because Congress said it was a “dollar.” Today’s Congress, however, assumes that the “dollar” need have no rational relationship to a weight of silver, of gold, or even of base metals. Thus, today’s Congress assumes that the value of money has nothing to do with the substance that composes a coin, but is merely the product of a political decree. In today’s Washington, D.C., might not only makes right, but also creates economic value!

Many of the same people who served in the Continental Congress participated in the Federal Convention that drafted the Constitution. And even those members of the Convention who had not served in the Continental Congress knew what that Congress had done. Therefore, when the Convention used the noun “dollar” in Article 1, Section 9. Clause I of the Constitution, it was with the tacit understanding of all the history surrounding that noun. Thus, the lesson here is clear: The constitutional “dollar,” the constitutional “Money-Unit” or “Money of Account” of the United States, is an historically determinate, fixed weight of fine silver in the form of a coin—in essence, a unit of measure—adopted, not created, first by the American market and then by the Continental Congress well before ratification of the Constitution.

c. Adoption of the “dollar” as the unit of money immediately after the ratification of the Constitution. Upon ratification of the Constitution. Congress and the Executive began work on a national monetary system.

(1) Alexander Hamilton’s Report on the Mint. On 28 January 1791, Secretary of the Treasury Alexander Hamilton presented to Congress his Report on the Subject of a Mint. “A plan for an establishment of this nature,” he wrote, “involves a great variety of considerations intricate, nice, and important.” Indeed, the erection of a mint was essential to the continued integrity of the nation’s coinage:

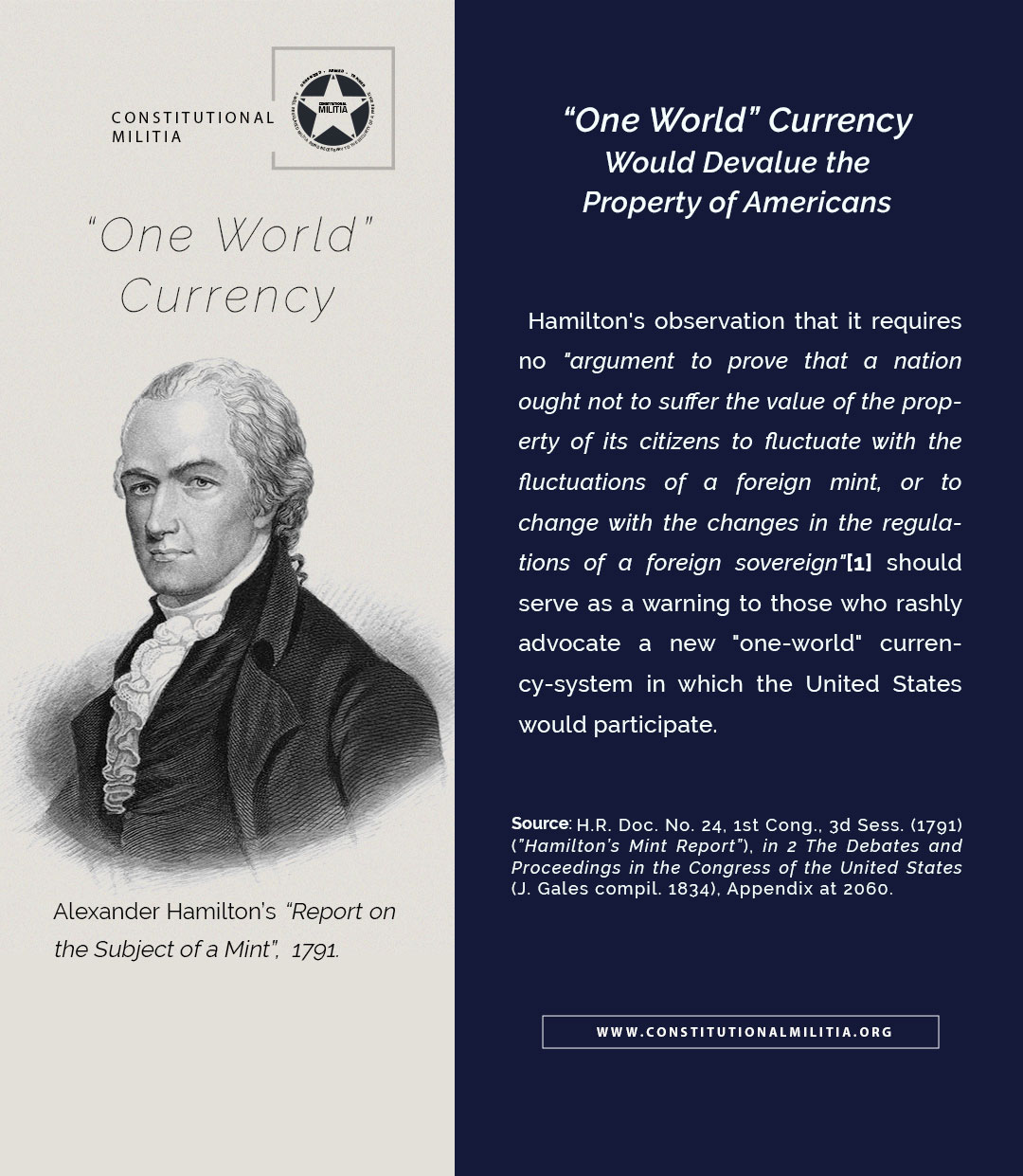

The dollar originally contemplated in the money transactions of this country [i.e., the silver Spanish milled dollar], by successive diminutions of its weight and fineness [in the Spanish mints], has sustained a depreciation of five per cent, and yet the new dollar has a currency in all payments in place of the old, with scarcely any attention to the difference between them. The operation of this in depreciating the value of property depending upon past contracts, and * * * of all other property, is apparent. Nor can it require argument to prove that a nation ought not to suffer the value of the property of its citizens to fluctuate with the fluctuations of a foreign mint, or to change with the changes in the regulations of a foreign sovereign. This, nevertheless, is the condition of one which, having no coins of its own, adopts with implicit confidence those of other countries.

* * * * *

It was with great reason, therefore, that the attention of Congress, under the late Confederation, was repeatedly drawn to the establishment of a mint; and it is with equal reason that the subject has been resumed * * * .[35]

To form “a right judgment of what ought to be done,” Hamilton posed two questions, “lst. What ought to be the nature of the money unit of the United States?,” and “2d. What the proportion between gold and silver, if coins of both metals are to be established?”[36]

Recognizing that “[a] pre-requisite to determining with propriety what ought to be the money-unit of the United States” is “to form as accurate an idea as the nature of the case will admit, of what it actually is,” Hamilton referred to the resolutions of the Continental Congress on the subject, noted that they had resulted in “no formal regulation on the point,” and concluded that “usage and practice * * * indicate the dollar as best entitled to that character.” As to “what kind of dollar ought to be understood; or, * * * what precise quantity of fine silver,” he surveyed the various pieces in circulation over the years, and recommended that “[t]he actual dollar in common circulation has * * * a much better claim to be regarded as the actual money unit.”[37]

Hamilton recognized that “[t]he suggestions and proceedings hitherto have had for object the annexing of [the title of ‘money unit’] emphatically to the silver dollar.” Yet, his personal view was that “a preference ought to be given to neither of the metals for the money unit”—at least “[i]f each of them be as valid as the other in payments to any amount.” He realized, of course, that adopting equivalent, interchangeable “money units” of both silver and gold would pose practical problems “from the fluctuations in the relative [market-]value of the metals”; but he suggested that this could be overcome “if care be taken to regulate the proportion between them with an eye to their average commercial value.”[38]

Turning to “the proportion which ought to subsist between [gold and silver] in the coins,” Hamilton proposed two “option[s]”: namely, “[t]o approach as nearly as can be ascertained, the * * * average proportion * * * in * * the commercial world”; or “[t]o retain that which now exists in the United States.” The first alternative “requir[ing] better materials than are possessed, or than could be obtained without an inconvenient delay,” he recommended instead the domestic market-ratio of “about as 1 to 15.” “There can hardly be a better rule in any country for the legal than the market proportion,” he explained, “if this can be supposed to have been produced by the free and steady course of commercial principles. The presumption in such a case is that each metal finds its true level, according to its intrinsic utility, in the general system of money operation.”[39]

In the course of determining the method by which the government would defray the expenses of coining silver and gold brought to the mint byprivate parties (the system of “free coinage”[40]), Hamilton restated the traditional policy against monetary debasement in emphatic terms:

[R]aising the denomination of the coin [is] a measure which has been disapproved by the wisest men in the nations in which it has been practiced, and condemned by the rest of the world. To declare that a less weight of gold or silver shall pass for the same sum, which before represented a greater weight, or to ordain that the same weight shall pass for a greater sum, are things substantially of one nature. The consequence of either of them is to degrade the money unit; obliging creditors to receive less than their just dues, and depreciating property of every kind.

* * * * *

The quantity of gold and silver in the national coins, corresponding with a given sum, cannot be made less than heretofore without disturbing the balance of intrinsic value, and making every acre of land, as well as every bushel of wheat, of less actual worth than in time past. * * *

[A debasement would cause] a rise of prices proportioned to the diminution of the intrinsic value of the coins. This might be looked for in every enlightened commercial country; but, perhaps, in none with greater certainty than in this; because in none are men less liable to be the dupes of sounds; in none has authority so little resource for substituting names for things.

A general revolution in prices * * * could not fail to distract the ideas of the community, and would be apt to breed discontents as well among those who live on the income of their money as among the poorer classes of the people, to whom the necessaries of life would * * * become dearer.

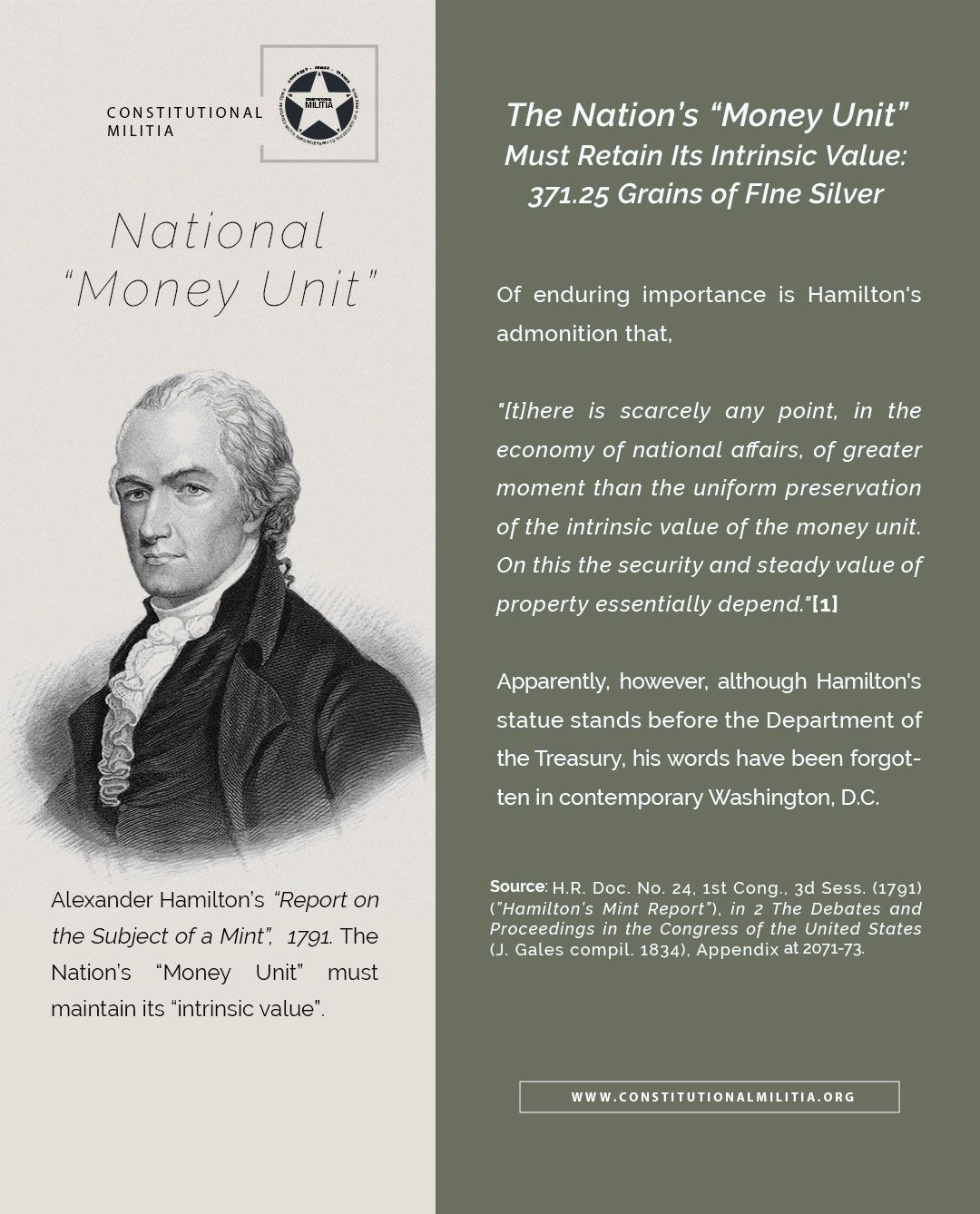

Among the evils attendant on such an operation are these: creditors, both of the public and of individuals would lose a part of their property, public and private credits would receive a wound; the effective revenues of the Government would be diminished. There is scarcely any point, in the economy of national affairs, of greater moment than the uniform preservation of the intrinsic value of the money unit. On this the security and steady value of property essentially depend.[41]

In sum, Hamilton recommended two equivalent statutory money-units based on weight, a gold coin of 24.75 grains of fine gold, and a silver coin of 371.25 grains of fine silver. “[N]othing better,” he wrote, “can be done * * * than to pursue the track marked out by the resolution [of the Continental Congress] of the 8th of August, 1786.”[42]

Hamilton’s Report thus restated the traditional monetary principles of American law, as the Continental Congress applied them, and as the Federal Convention embodied them in the Constitution. Congress, Hamilton urged, should adopt silver and gold as the nation’s monetary substances, at an exchange-ratio representing the average proportionate value between the metals in the domestic free market. Congress should continue on “the track marked out” under the Articles of Confederation and the Constitution by employing the “dollar” as the “money-unit,” or “money of account”—a silver “dollar” derived directly from the Spanish milled dollar, and a new gold coin containing a silver—”dollar’s” worth of gold. The government should provide “free coinage” of both silver and gold for the public. And it should guarantee the preservation of the intrinsic value of the coinage.

Of enduring importance is Hamilton’s admonition that “[t]here is scarcely any point, in the economy of national affairs, of greater moment than the uniform preservation of the intrinsic value of the money unit. On this the security and steady value of property essentially depend” Apparently, however, although Hamilton’s statue stands before the Department of the Treasury, his words have been forgotten in contemporary Washington, D.C.

(2) The Coinage Act of 1792. Little more than a year after Hamilton’s Report, Congress enacted its principles into law. The Coinage Act of 1792[43] initiated a new statutory system embodying the constitutional principles that Hamilton had reaffirmed. First, Congress followed consistent American common-law tradition by continuing the use of silver, gold, and copper as “Money.”[44] Second, it reiterated the judgment of the Continental Congress and the Constitution that “the money of account of the United States shall be expressed in dollars or units,”[45] and defined the “DOLLARS OR UNITS” in terms of weight, as “of the value of a Spanish milled dollar as the same is now current, and to contain three hundred and seventy-one grains and four sixteenth parts of a grain of pure * * * silver.”[46]

Recognizing that to adopt Hamilton’s suggestion of a “gold dollar” would cause confusion and require constant governmental supervision to “regulate * * * Value[s],”[47] Congress created no such coin, instead mandating the coinage of “EAGLES,” “each to be of the value of ten dollars or units,”[48] that is, of the weight of fine gold equivalent in the marketplace to 3,712.50 grains of fine silver. Following Hamilton’s recommendation, though, it fixed “the proportional value of gold to silver in all coins which shall by law be current as money within the United States” at “fifteen to one, according to quantity in weight, of pure gold or pure silver.”[49] And it made “all the gold and silver coins * * * issued from the * * * mint * * * a lawful tender in all payments whatsoever, those of full weight according to the respective values [established in the Act], and those of less than full weight at values proportional to their respective weights.”[50]

Thus, Congress did not establish a “gold dollar,” or enact a “gold standard,” as the popular misconception holds. For example, the Encyclopaedia Britannica erroneously reports that the “dollar * * * was defined in the Coinage Act of 1792 as either 24.75 gr. (troy) of fine gold or 371.25 gr. (troy) of fine silver.”[51] The Act did no such thing. It explicitly defined the “dollar” as a fixed weight of silver, and “regulate[d] the Value” of gold coins according to this standard unit (or money of account) and the market exchange-ratio between the two metals. Nowhere did the Act refer to a “gold dollar,” only to various gold coins of other names that it valued in “dollars.”[52]

Congress also provided free coinage “for any person or persons,”[53] and affixed the penalty of death for the crime of debasing the coinage.[54]

Thus did the first Congress—which knew what the Constitution meant if any Congress ever did—rigorously apply the Constitution’s mandate: It determined as a fact “the value of a Spanish milled dollar as the same is now current,” and thereby permanently fixed the constitutional standard of value, or “money of account,” as a unit of weight consisting of 371.25 grains of fine silver in the form of coin. It coined American “dollars” as “Money,” containing this intrinsic value of silver. It coined American “eagles” as “Money,” containing a fixed weight of pure gold—and regulate[d]” their “Value” at so-many “dollars” by comparing their intrinsic value in (weight of) fine gold to the market-equivalent of silver. It gave both the silver and gold coins legal-tender character for their intrinsic values in all payments. It opened the mint to free coinage of the precious metals. And it outlawed debasement of the nation’s new “Money.”

The handiwork of the statesmen who drafted and approved these measures is more than a merely coincidental embodiment of the traditional principles of Anglo-American common law, the experiences of the Continental Congress, and the explicit provisions of the Constitution. Rather, taking into account the vicissitudes of the time, the Coinage Act of 1792 perfectly reflects what the common law and the law under the Articles of Confederation had been before ratification of the Constitution, and what the constitutional law was then and remains today.[55] It is a definitive interpretation, elaboration, and application of the Constitution—with, in some of its sections at least, a clearly constitutional character of its own: in particular, Sections 9 (definition of the “dollar”), 14-15 (free coinage of silver and gold), 16 (legal-tender character for silver and gold coins),[56] and 20 (“dollar” identified as the “money of account”).[57]

Most importantly, Congress’ determination of the proper weight of the “dollar” is, for all practical purposes today, a statement of constitutional law unalterable except by amendment of the Constitution itself. For, at the remove of almost two centuries, to check the accuracy of the conclusion that 371.25 grains (troy) of fine silver best represents an average weight of the various Spanish milled “dollars” in circulation in the United States in 1792 is most probably impossible.

Conclusion

In the light of this history, the present monetary provisions of the United States Code demonstrate that official Washington, D.C., has no conception of what a “dollar” really is. The reason for this self-imposed ignorance is obvious. By reducing the “dollar” to a political abstraction, the national government has empowered itself to engage in limitless debasement (depreciation in purchasing power) of the currency. A “dollar” that contains—and must perforce of the Constitution contain—371.25 grains of fine silver cannot be reduced in value below the market exchange value of silver for other commodities. A pseudo-“dollar” that contains no fixed amount of any particular substance per “dollar” can be reduced in value infinitely. As debasement of currency amounts to a hidden tax, Congress’ silent refusal to recognize the constitutional “dollar” amounts to the usurpation of an unlimited power to tax through manipulation of the monetary system. Thus, modern “money” has become a means for the total confiscation of private property by the government.

More ominously, this scheme of surreptitious confiscation remains hidden from the vast majority of Americans, who seem blissfully unconcerned about the issue most important to the soundness of the country’s monetary system: namely, the character of the monetary unit. One need not be overly pessimistic to predict that misuse by politicians of the fictional, constantly depreciating pseudo-“dollar” to expropriate unsuspecting citizens will continue until an economic crisis finally shocks an increasingly impoverished American people out of its slumber, and forces the people to ask the simple question: “What is a ‘dollar’?” At that time, the answer will be no different from what it is today, and has been since 1704—but the opportunity to use that knowledge to prevent a catastrophe may be long gone.

Therefore, those few who do know what a “dollar” is, and why that definition is important, need to inform as many of their fellow-citizens as possible. If time has not already run out for re-education of the American people in this area, it is racing towards the historic exit. Under these circumstances, silence by the friends of sound money and honest government is not “golden,” but potentially fatal.

{kind=link}